Close

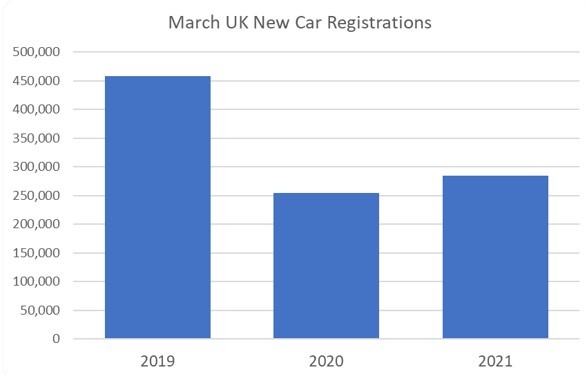

CloseNew car registrations in March showed the first green shoots of growth since August 2020, with 29,280 more units registered compared to the same month last year. This represents an increase of 11.5% according to figures published by the Society of Motor Manufacturers and Traders (SMMT).

However, March is also the anniversary of the first full lockdown caused by the COVID-19 pandemic, so comparisons with 2020 figures will fluctuate wildly throughout the year. If compared to March 2019’s pre-pandemic normal market, March 2021 registrations fell 38%.

Data courtesy of SMMT

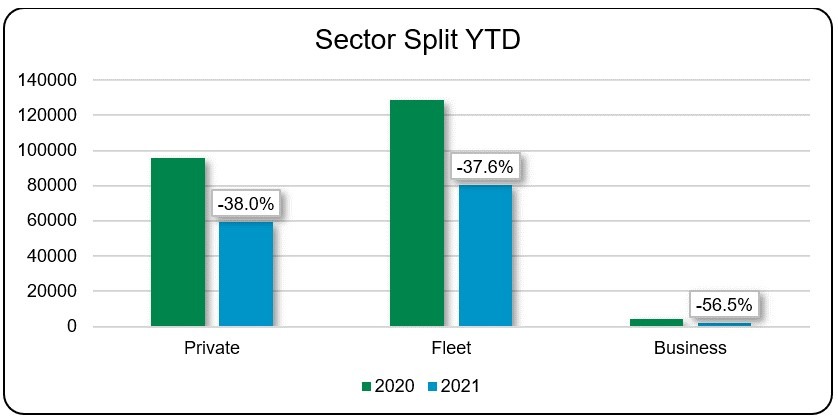

The March on March growth figure was not uniform across all sectors. While Fleet volume grew 28.7% or 33,784 units and Business was up 18.6% or 902 units, sales to private consumers fell 4.1% or 5,406. In March 2020, the Fleet and Business sectors suffered larger falls in registrations than retail, so had a lower base point to grow from. Besides, many lease contract extensions have expired, hence an uptick in March registration activity, as company cars are often ordered without any physical viewing. Private consumers are more likely to purchase a vehicle after visiting dealerships first, which is why the April 12 reopening of non-essential retail is so important for the new and used car markets.

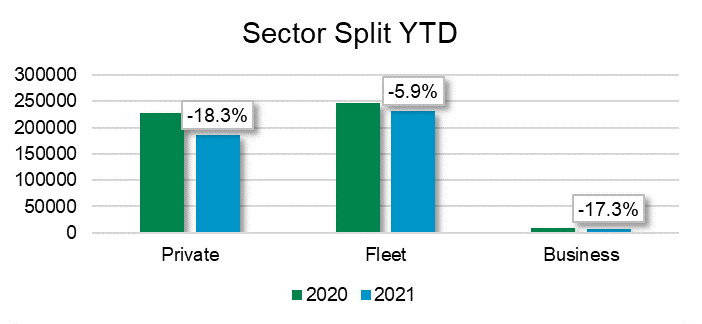

Despite March’s rise in registrations, the new car market dropped by 58,032 cars or 12% in quarter one, with sales to private consumers affected most as shown in the chart below.

Data courtesy of SMMT

The shift to alternative fuelled cars is continuing at pace, with plug-ins making record volume. Battery electric vehicles (BEVs) and plug-in hybrid vehicles (PHEVs) took a combined market share of 13.9%, up from 7.3% last year, as the choice available to customers continues to grow. Registrations of BEVs increased by 88.2% to 22,003 units, while PHEVs rose by 152.2% to 17,330. Hybrid electric vehicles (HEVs) also rose 42.0% to reach 21,599 registrations.

For this positive trend to continue, the government needs to maintain customer incentives for new cleaner technologies, whilst planning and implementing improved infrastructure to cope with the increasing registrations.

As we look ahead to the second quarter, it is logical that the new car market will catch back some of the ground lost in Q1, as the market was effectively closed in April and May last year due to Lockdown-1, with only just over 24,400 cars registered in the two months combined.