Close

CloseAs 2020 ends, it has been a ghastly year for so many people in private and in business terms, possibly the worst year they have ever had. However, for businesses involved in the buying and selling of used light commercial vehicles (LCVs), 2020 has told a different story.

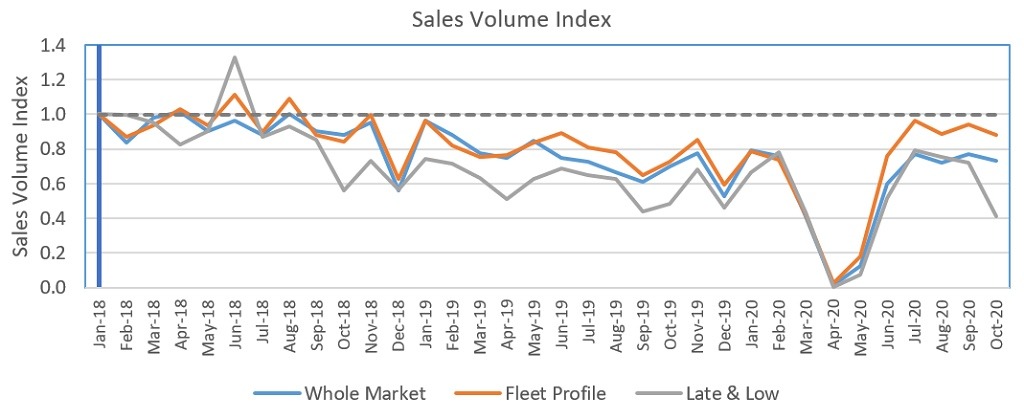

Back in January, the LCV Market started as predicted, taking a week to shake off Christmas excesses before picking up pace with strong prices paid for the nicest stock. Strong trading continued until mid-March when Lockdown-1 arrived, stopping the country in its tracks.

Everything stopped. Factory production lines ground to a halt, suppliers didn’t supply, no new vehicles were delivered to customers, no auctions were open for sales and for the trade to have a brew beforehand and no used LCVs were bought at dealerships.

As the country sat at home ordering PPE and emergency supplies, food, groceries and everything else on the web, delivery companies realised that ‘if they ordered it, they’d need more LCVs to deliver it’. Immediately, searches on classified LCV sales websites rose dramatically and traders’ phones started to ring. The demand for more LCVs leapt to cover the delivery of the huge increase in essential equipment and products. As the country was urged to stay at home, home shopping went through the roof, causing delivery companies to report a Christmas-like spike in demand.

The demand for additional vehicles swallowed the majority of existing dealer stock, forcing the Government to help the sector by rapidly legislating temporary relaxations of delivery restrictions and drivers’ hours.

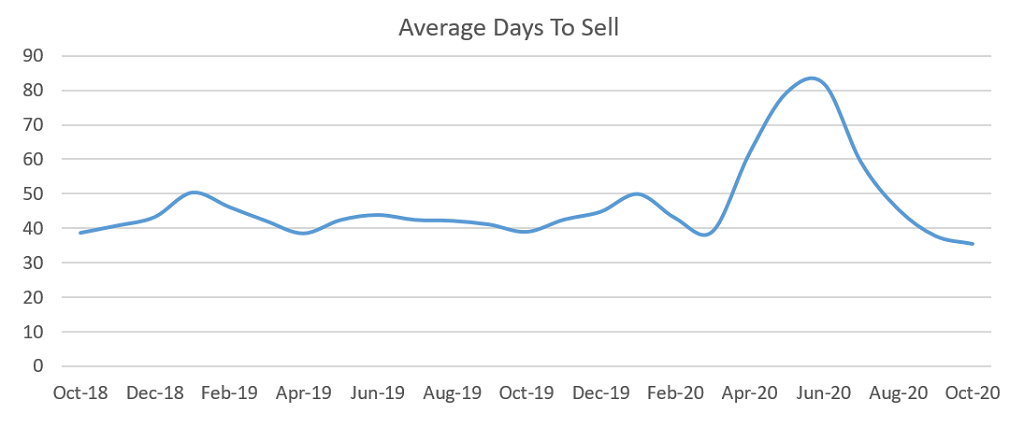

Businesses with existing fleets who would usually be de-fleeting during the summer did not. Most had little choice, but to run vehicles for longer, as there was no new stock to replace them with. In turn, this meant there was a smaller pool of second-hand stock being returned to the used market.

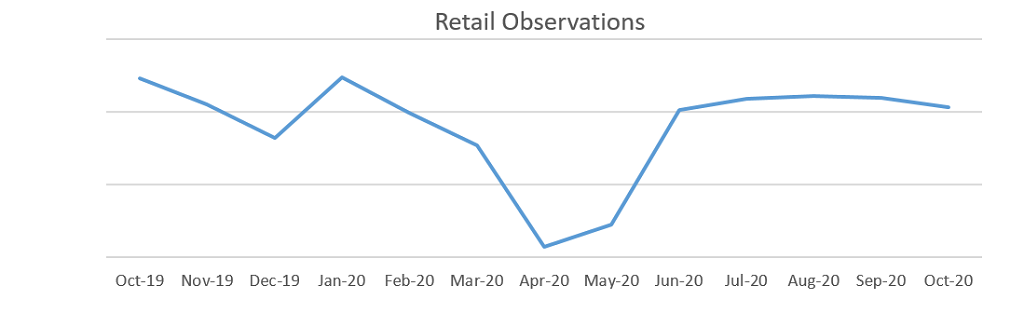

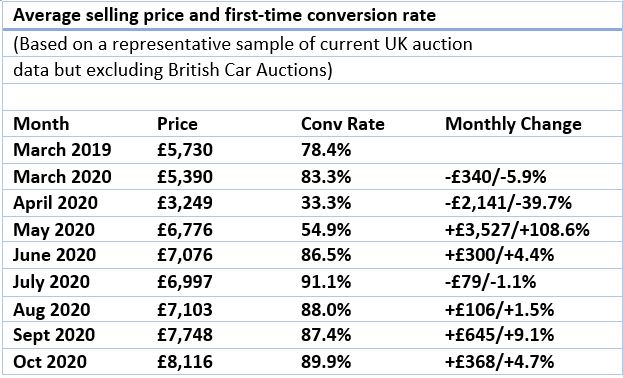

May saw the restart of LCV auctions, albeit only in an online format. The trade adjusted quickly, accepting the online sale process of buying remotely with the help of a series of images. The reopening of the auction houses coincided with pent-up retail demand with the initial oversupply leading to a short-term spike in transactions. This was soon replaced by supply shortages that started to starve the market of new and used stock. With customers in desperate need of additional vehicles, prices started to rapidly increase as the nicest examples across all ages were sought out.

The government had also offered small business loans and grants to help operators through the pandemic. This money was often spent on a newer van and with fewer vans for sale, this added to the unparalleled demand in the used market, sending prices even higher.

Demand has hardly faltered since Lockdown-1 maintaining prices at record high levels. Now as Lockdown-2 progresses, there is still no real sign of weakness in the used market.

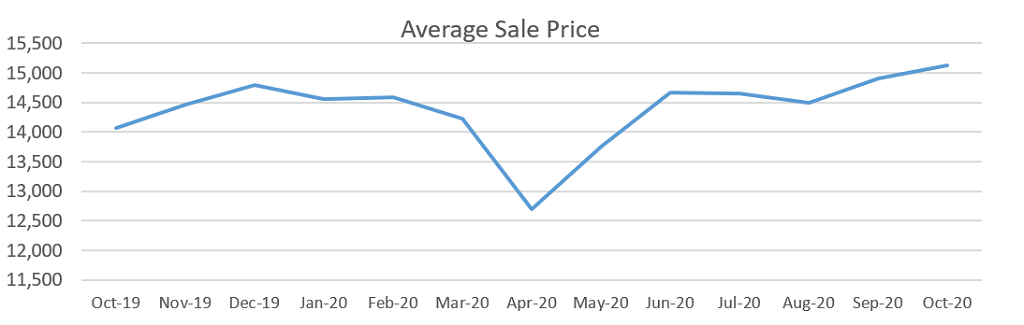

In March 2019 the average selling price was £5,730, only £340 higher than March 2020. However, by October, the average selling price had shot up to £8,116, an increase of £2,726 or 33.6% over the 7 months of the pandemic.

June recorded an average sale price of over £10,750 for Euro 6 compliant LCVs, whilst pre-Euro 6 stock made up over 55% of all sales, selling for an average price of nearly £5,200. Of those who purchased a vehicle, 25% had never purchased online before.

By August, the average Euro 6 sales price had risen to over £11,400, whilst the Euro 5 and older vehicles had risen to more than £5,750.

By October, pre-Euro 6 values looked to have peaked, however, average prices for Euro 6 vehicles rallied again to nearly £12,775 despite increases in both age and mileage. The sustained appetite for retail-ready stock shows no sign of abating, with newer used vehicle prices likely to track Brexit driven new price increases.

Looking further ahead to the remainder of 2020 and into 2021, there will be several factors impacting the sector and the wider economy.

Continued UK economic recovery needs to take into account the currently unknown factors of a successful vaccination programme against COVID -19 and Brexit. The possibility of 10% tariffs looms large on new vehicle list prices and 4% on parts if no trade agreement is reached with the European Union before the end of the year.

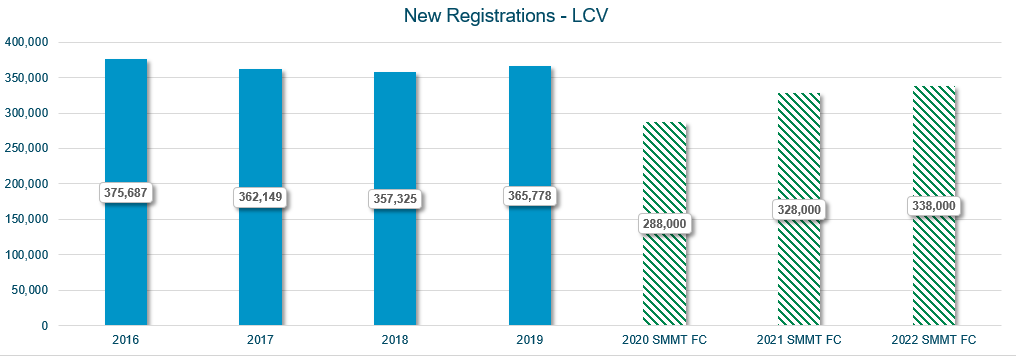

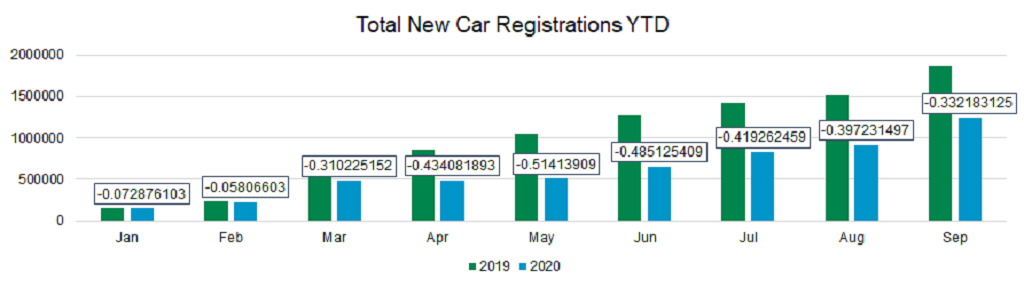

The quarter four Society of Motor Manufacturers and Traders (SMMT) LCV registration forecast for 2020 surprisingly estimated an increase of 6.6% to 288,000 units. Lead in delays on new stock, a shortage of vehicles at dealer level and two months left of the year would seem to rule out achieving those predictions. Registrations in the UK as at the end of October, remain over 24% below the same point last year.

Used LCVs will likely be the dominant revenue opportunity for dealers and OEMs for the remainder of the year and certainly the first half of 2021.

The new vehicle market is unlikely to return to any form of normality for some time, with registrations for 2021 tracking similarly to 2020. OEMs will bring forward strategy changes in line with the announcement that new petrol and diesel vans will no longer be sold from 2030. Manufacturers will accelerate the move to electric to respond to the new legislation and consumer demands.

Looking further ahead, bigger impacts upon the sector will include the clean air agenda, remote working and mobility. All will influence consumer choice with LCV fleets being increasingly chosen for specific urban, regional or national roles.

Glass’s continues to monitor the LCV market closely and has an open dialogue with auction houses and manufacturers, leasing and rental companies, independent traders and dealers as well as the main industry bodies. This information, combined with the wealth of knowledge in our CV team ensures Glass’s continue to be the most relevant in the market place.