Close

CloseAre regulations responsible for the fast pace of changes seen across the automotive market? Join Christof Engelskirchen, Autovista Group’s chief economist, Phil Curry, Daily Brief editor and journalist Tom Geggus in the latest Autovista Group Podcast to find out.

You can listen and subscribe to receive podcasts direct to your mobile device, or browse through previous episodes, on Apple, Spotify, Google Podcasts and search for Autovista Group Podcast on Amazon Music.

Show notes

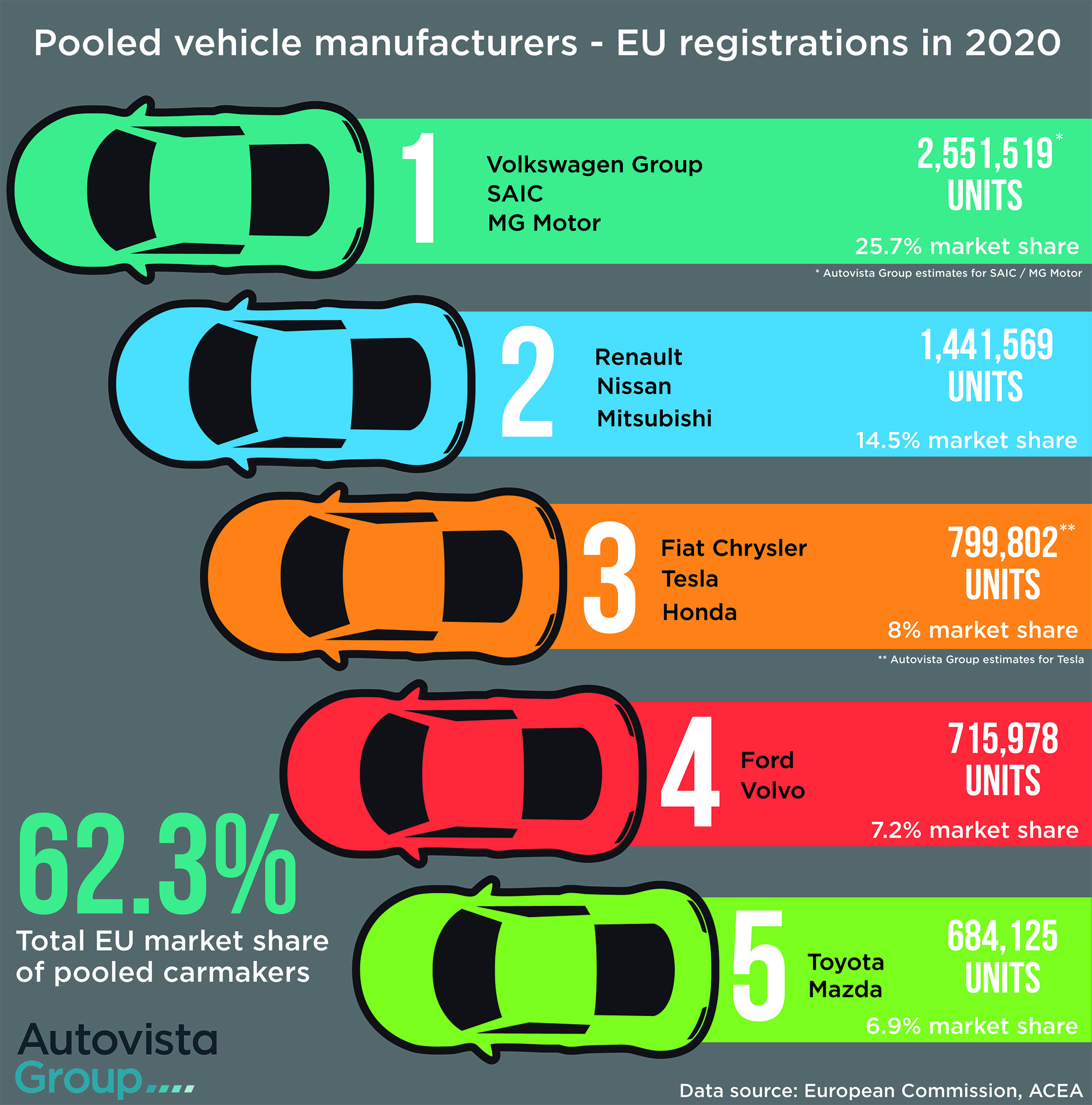

Carmakers successfully pooled emissions to meet 2020 EU targets

Hitting the target: Lone carmakers that successfully reduced their emissions

Swedish ICE ban would not drastically aid climate targets

Is the automotive industry waking up to hydrogen’s potential?

Are EVs as green as they seem?

Germany paves the way for adoption of autonomous vehicles

Podcast: Should Automated Lane-Keeping Systems be labelled ‘self-driving’?