Close

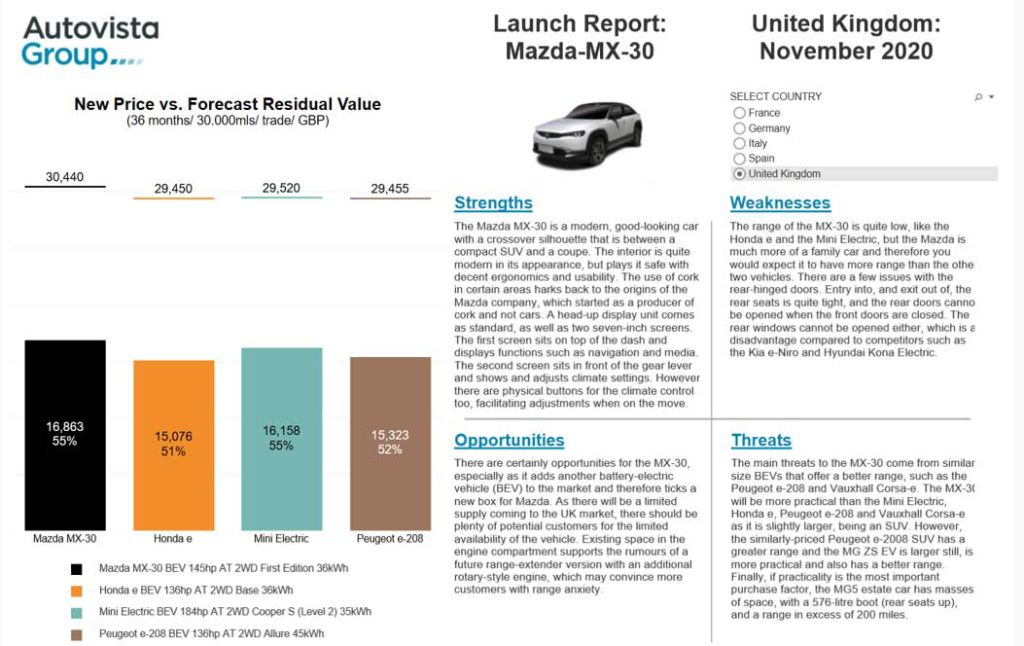

CloseThe new Mazda MX-30 has an innovative crossover style that is between a compact SUV and a coupe, with design elements such as rear-hinged doors, sharp-edged wheel arches, rear lights inspired by the MX-5 roadster, and a swooping roofline.

The modern, high-quality interior features a minimalist and well-finished dashboard, and standard equipment is comprehensive, including LED headlamps, satnav, and a head-up display. With a complete list of advanced driver-assistance systems (ADAS), safety is a strength of the MX-30, which has recently been awarded five stars by Euro NCAP.

The MX-30 charges to full battery capacity in good time, but the range of about 200km (WLTP) is relatively low, even compared to other models that are not fully charged. However, the purpose of the MX-30 is to present an eco-friendly vehicle, and the battery was selected as it has a lower impact on the environment in terms of CO2 emissions during production, as well as energy consumption. There are currently no versions with extended battery capacity, but space in the engine compartment supports rumours of a range-extender variant with an additional rotary-style engine.

List prices are typically slightly lower than for C-SUV rivals but higher than for electric hatchback models. In Germany, the €9,000 incentive for battery-electric vehicles (BEVs) gives an adjusted retail price from about €23,000, which is even on a par with the petrol-powered Mazda CX-30 C-SUV.

Click here or on the image below to read Autovista Group’s benchmarking of the Mazda MX-30 in France, Germany, Italy, Spain and the UK.

We present new prices, forecast residual values and SWOT (strengths, weaknesses, opportunities and threats) analysis.