Close

CloseThe new Hyundai Tucson has an assertive and bold design, with its front face combining the headlights and grille. The 3D rear-light signature echoes the progressive triangular headlight design and two-tone colour personalisation is now possible. As the new Tucson is longer and wider, it is roomier and more practical than its predecessor and has a large boot.

The modern and refined digital cockpit, featuring a flush-fitting 10-inch screen, is standard across the range and there is also a digital TFT screen directly in front of the driver. The materials, trim and build quality are all good and there are numerous ADAS and safety features, including a central airbag between the two front seats. A neat touch is the blind-spot monitoring system, which shows a digital feed from the left or right side of the car, depending on which direction is indicated.

The Tucson is offered with mild-hybrid (MHEV) petrol and diesel engines or as a full hybrid-electric vehicle (HEV), and a plug-in hybrid (PHEV) version will be available too. The trim lines are well composed and there are relatively few options, leading to well-equipped used cars.

With the leap forward in quality and roominess compared to its predecessor, the Tucson has the potential to attract a wider selection of consumers. The HEV version may present an attractive business proposition for buyers who are not yet ready to plug in.

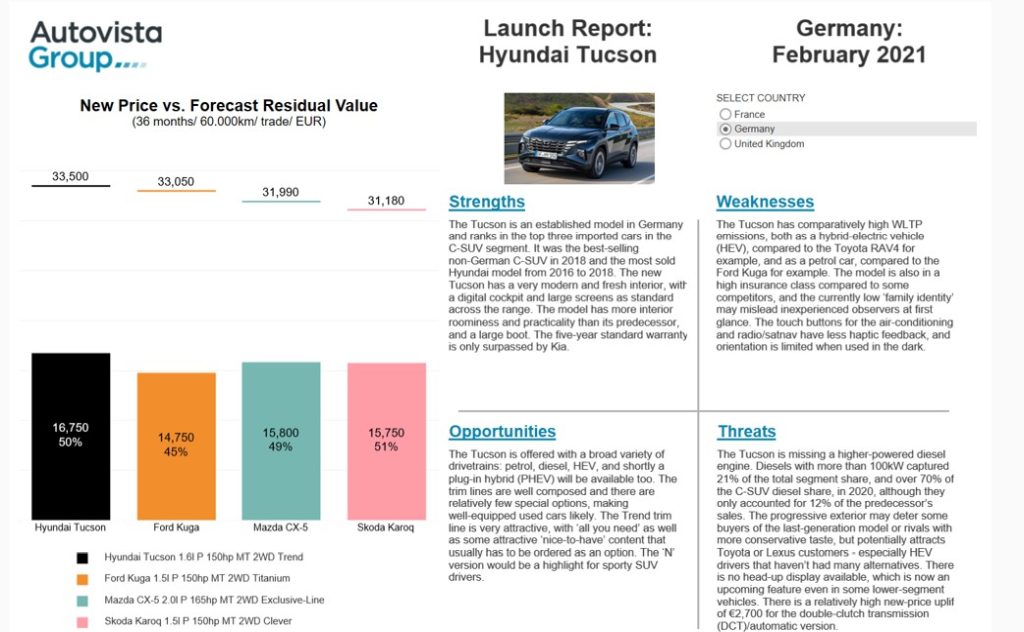

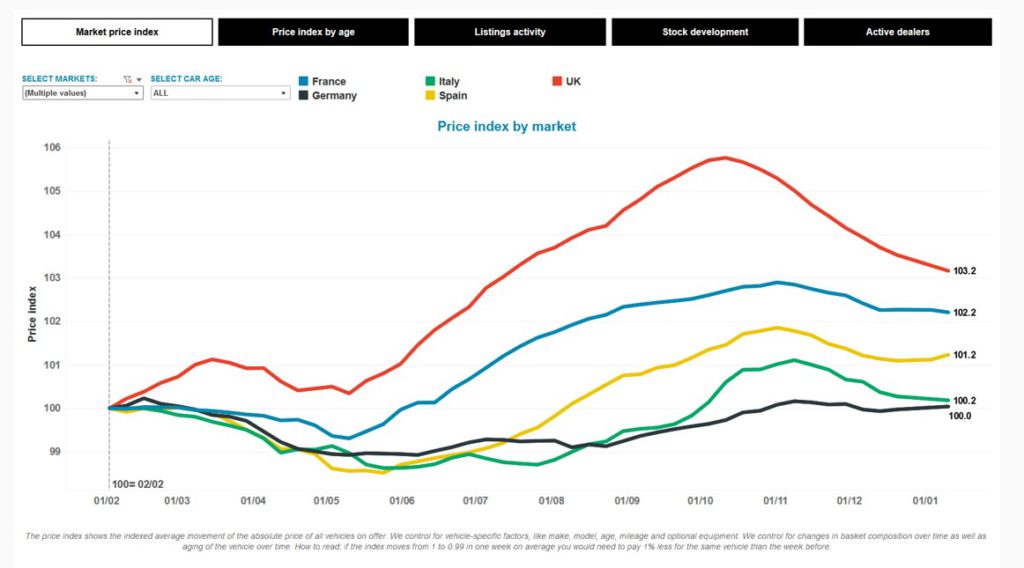

Click here or on the image below to read Autovista Group’s benchmarking of the Hyundai Tucson in France, Germany and the UK. The interactive launch report presents new prices, forecast residual values and SWOT (strengths, weaknesses, opportunities and threats) analysis.