Close

CloseAutovista Group Daily Brief editor Phil Curry discusses the registration figures from Europe’s big five automotive markets. While numbers may be down, the outlook for the whole year is more positive…

To get notifications for all the latest videos, you can subscribe for free to the Autovista Group Daily Brief YouTube channel.

Show notes

Lockdown drives German new-car registrations down by 19% in February

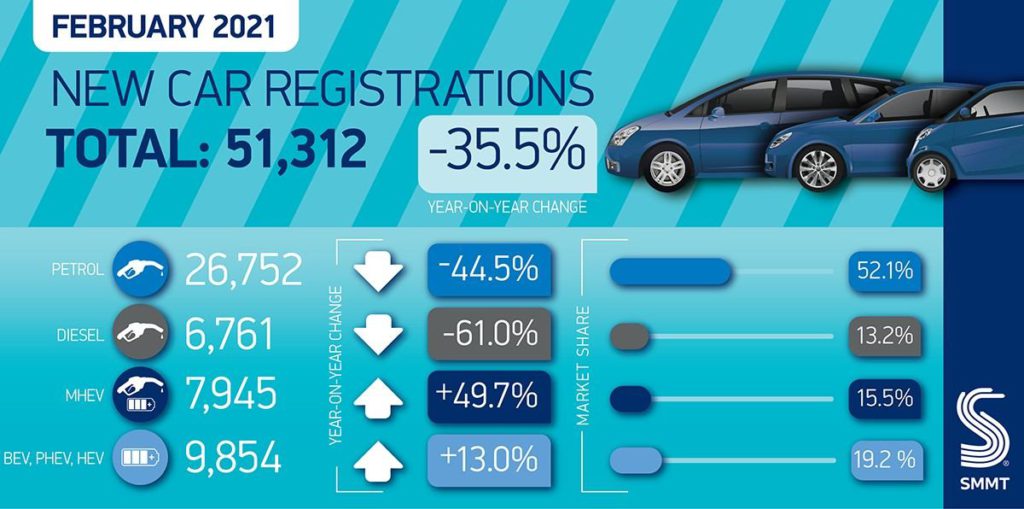

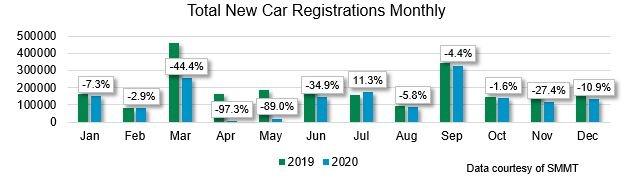

February UK new-car registrations plunge to level of 1959

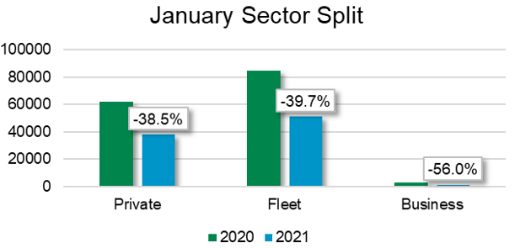

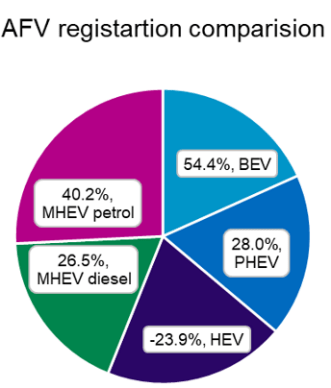

Significant downturns in European registrations in February