Close

CloseUsed Car Auction Wholesale Market

Finally over, 2020 will be remembered above all for a certain virus that wreaked havoc around the world and across our global industry. For a whole year, COVID-19 has affected every aspect of our lives and it will have a clear effect on 2021. Lockdowns, mask-wearing and travel restrictions, unimaginable this time last year, have become part of our life and have unsurprisingly impacted the UK’s car markets.

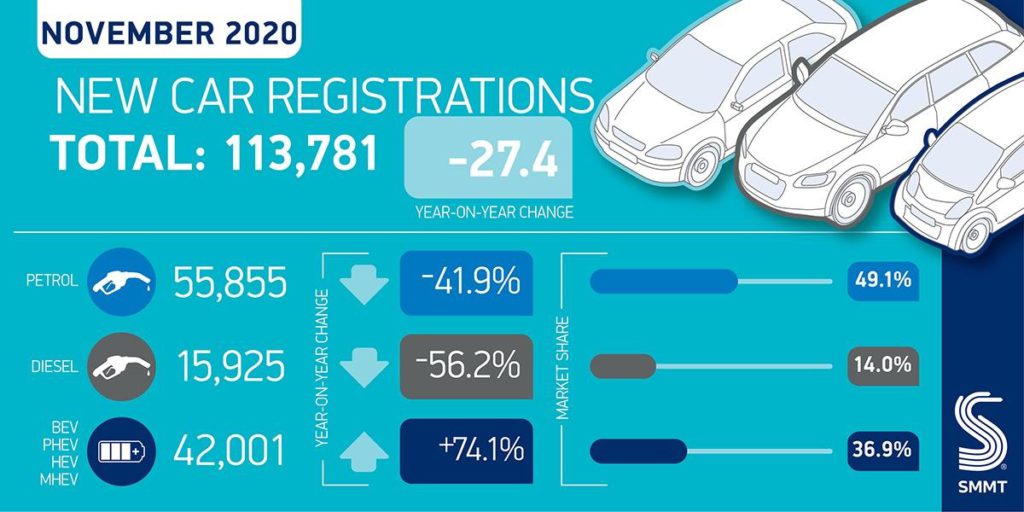

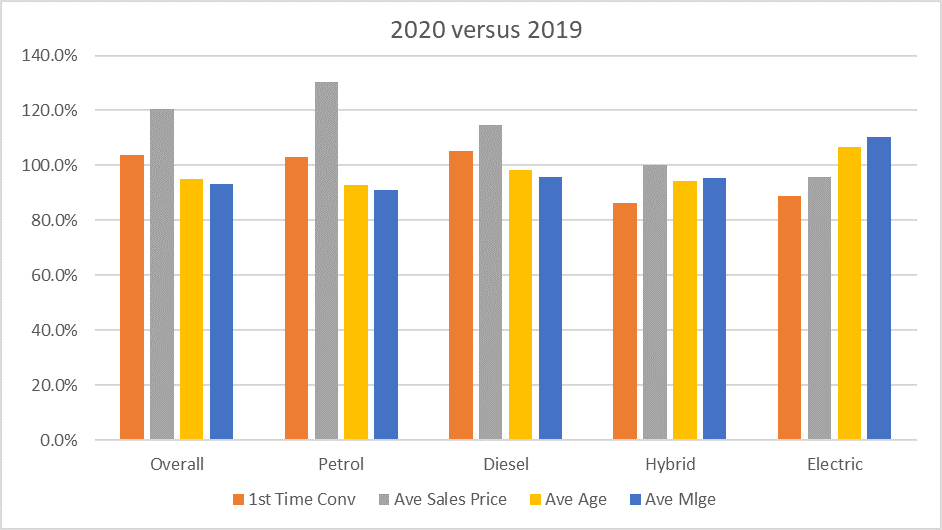

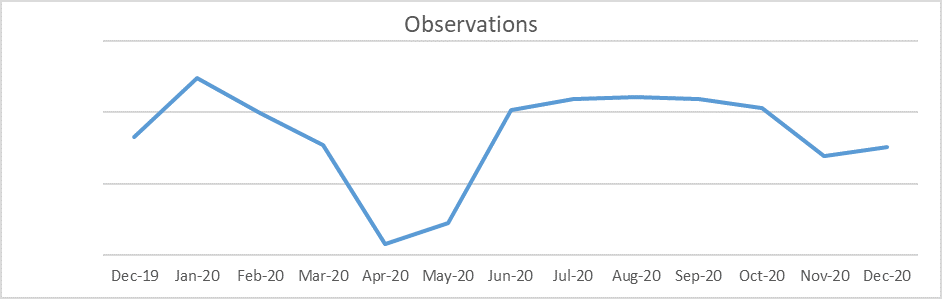

New car registrations were down almost 30% due to reduced demand and severely impacted new car supply. Used car sales were also down, although it was good to see how quickly the used car retail sales switched to safely distanced online sales processes. Due to the various travel and gathering restrictions, auction providers suspended physical sales and now rely entirely on online auction portals. Fortunately, buyers adapted quickly and whilst overall sales volume for 2020 was down from 2019, first-time conversion rates and average sales prices were both up versus 2019 (3.6% and 20.6% respectively).

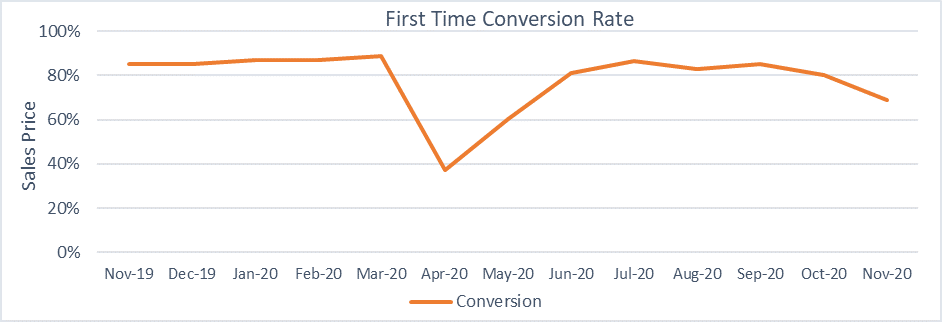

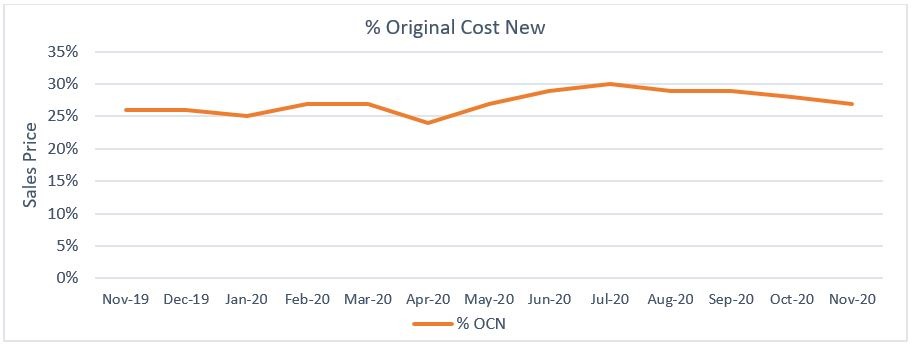

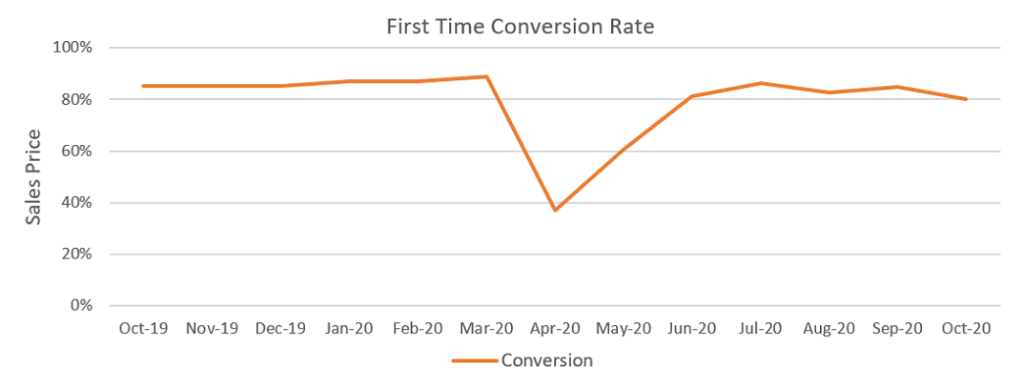

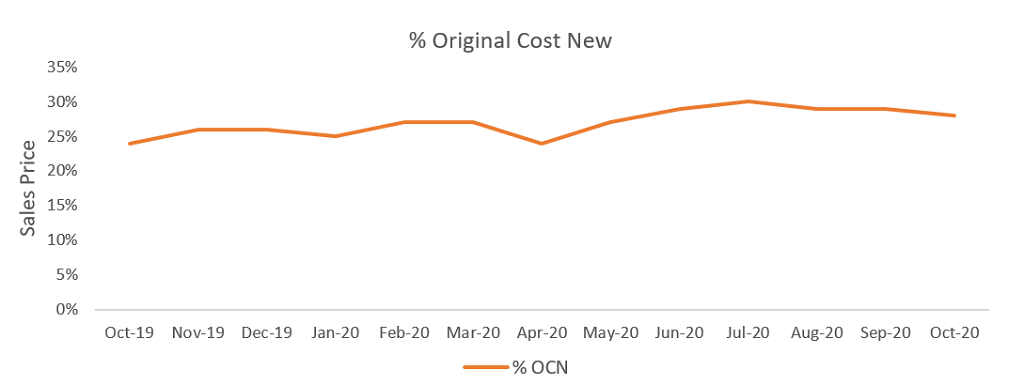

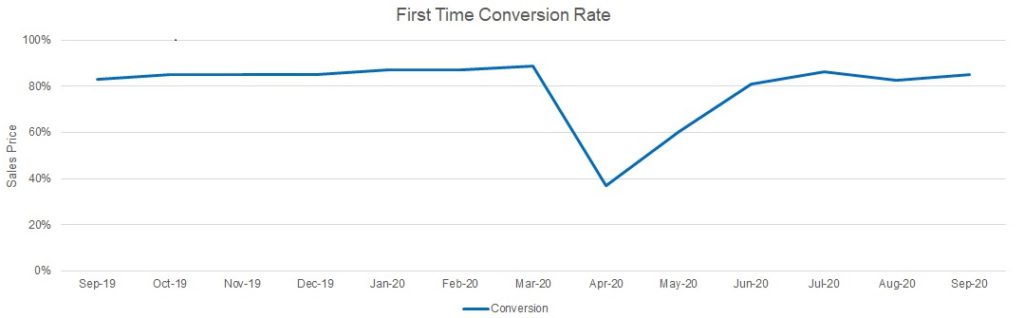

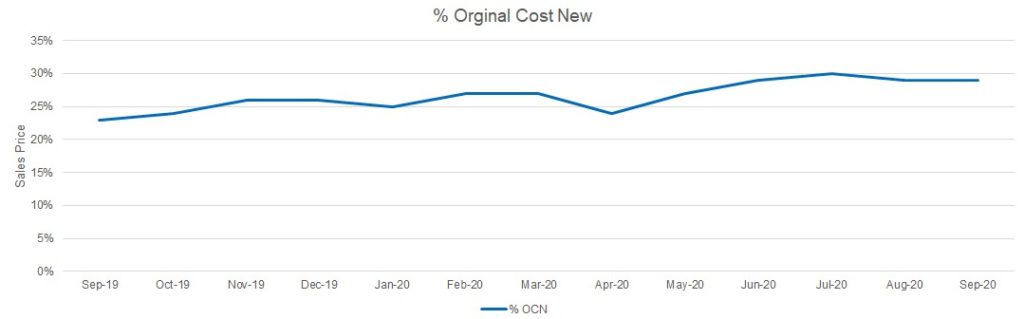

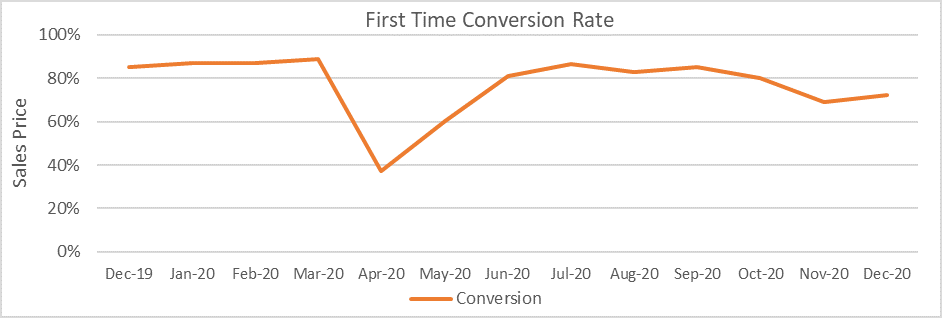

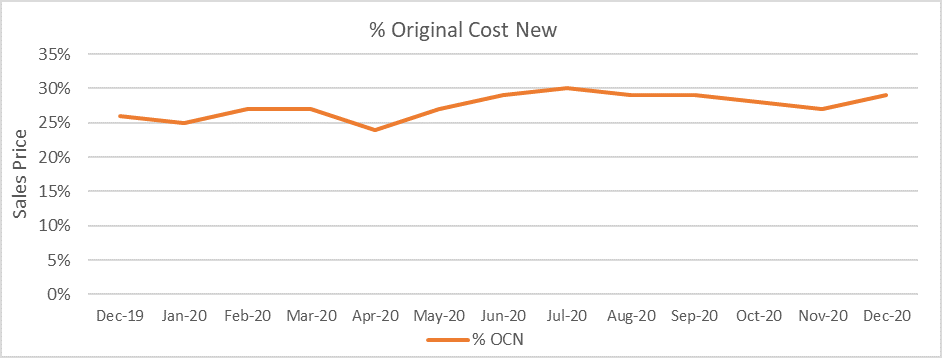

Specifically analysing December with Glass’s key metrics of first-time conversion rate and percentage of original cost new: the conversion rate of 72.4% was 5.2% higher than in November but almost 13% lower than the 85.3% achieved in December 2019. The average percentage of the original cost new was up 3.0% and 7.4% against November 2020 and December 2019 respectively. These results reflect the trends seen throughout the year, fewer cars selling with values holding up well. Given the circumstances, this is more positive than the expectations suggested.

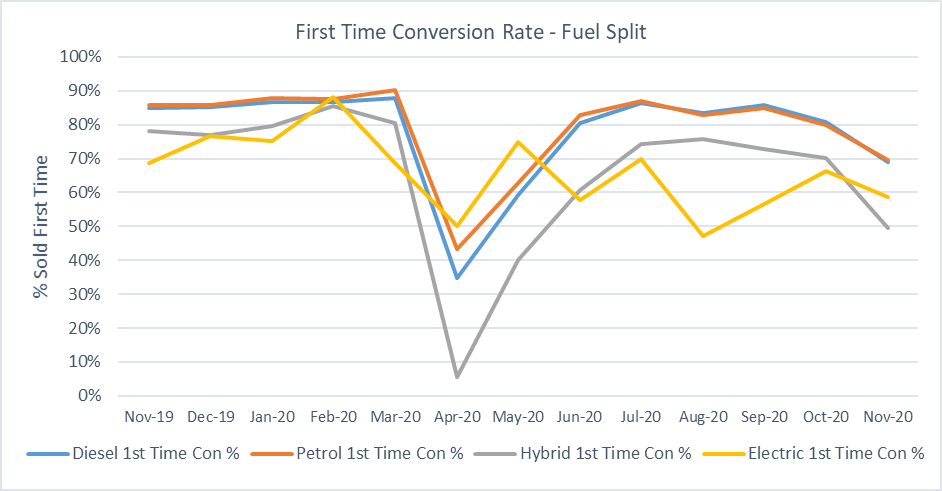

Despite their increasing popularity in the new car market, demand for HEVs (Hybrid Electric Vehicles) and BEVs (Battery Electric Vehicles) at auction continues to be lower than their ICE (Internal Combustion Engine) equivalents. Additionally, cars that require preparation work or are lack specification are also proving less desirable. This trend became more apparent as 2020 progressed. It appears buyers will still pay good money for the “right” stock, however, as times are more challenging, buyers are less keen to buy cars requiring additional preparation or that are outside of their comfort zones.

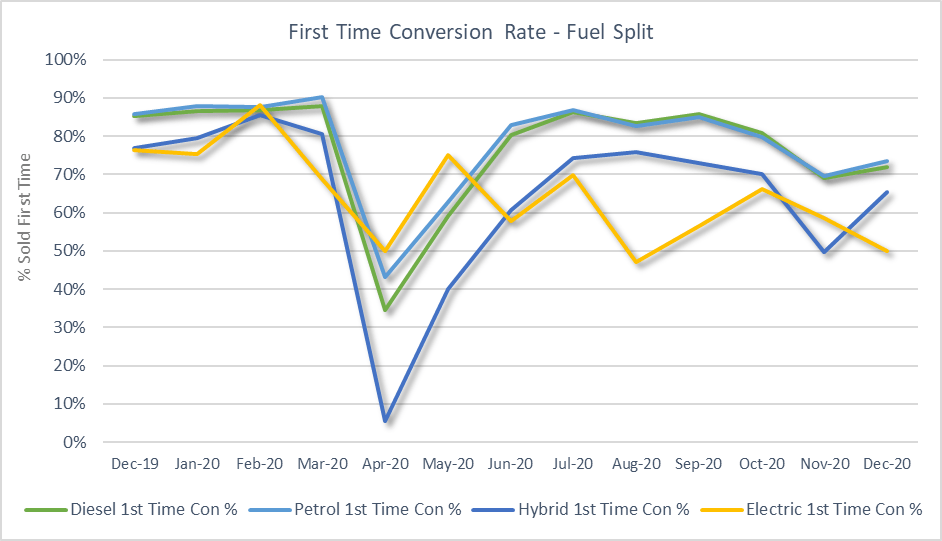

The graph below shows first-time conversion rate by fuel type and indicates that buyers are still more comfortable buying petrol and diesel cars rather than alternative fuel types. Petrol and diesel-powered cars achieve virtually the same conversion rates, with hybrids scoring a lower value and BEVs most susceptible to changes in supply and demand.

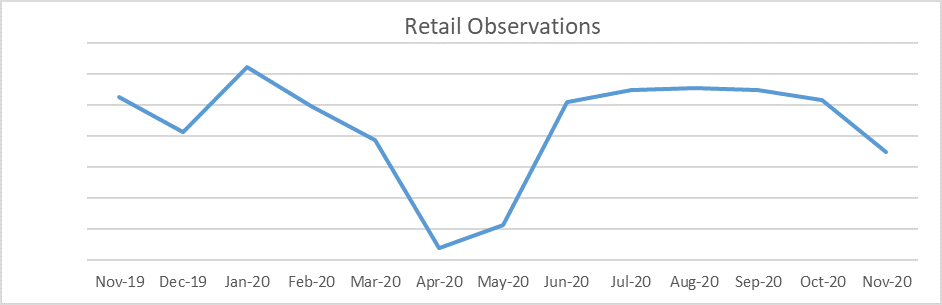

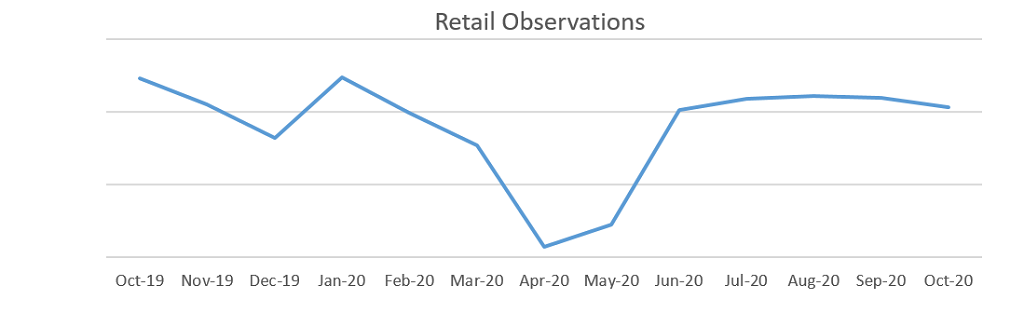

Used Car Retail Market

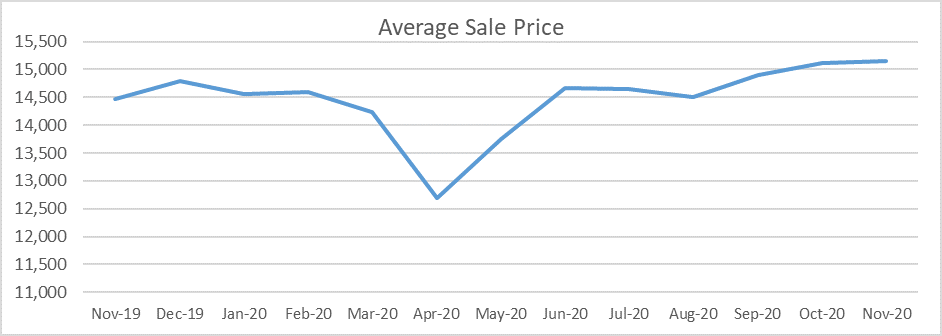

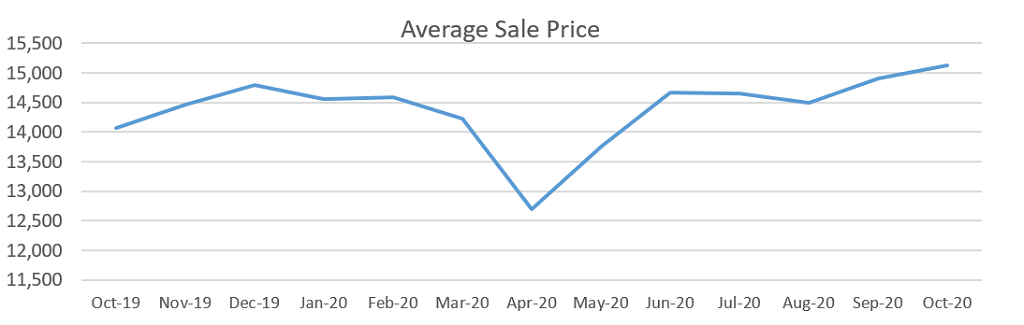

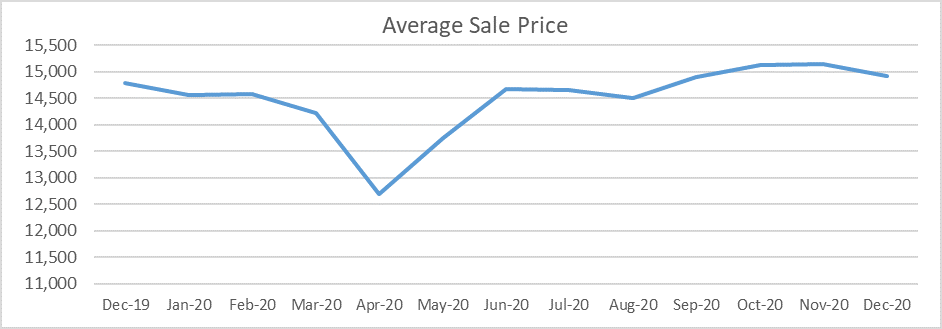

December is traditionally a three-week month due to the festive break. With the challenges of the November lockdown in England and other restrictions across the UK, the number of used car retail sales was 7.9% lower than December 2019 and increased 9.4% versus November 2020. Interestingly, whilst the average sale price was not too dissimilar to the averages for November 2020 and December 2019 – 1.5% higher and 0.8% lower – the average age of the cars sold, at 49.4 months, was 1.8 months younger than November but a notable 9.4 months older than in December 2019.

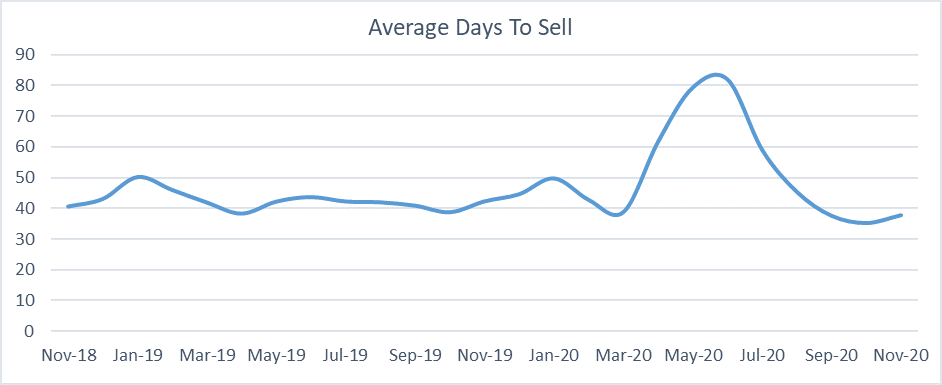

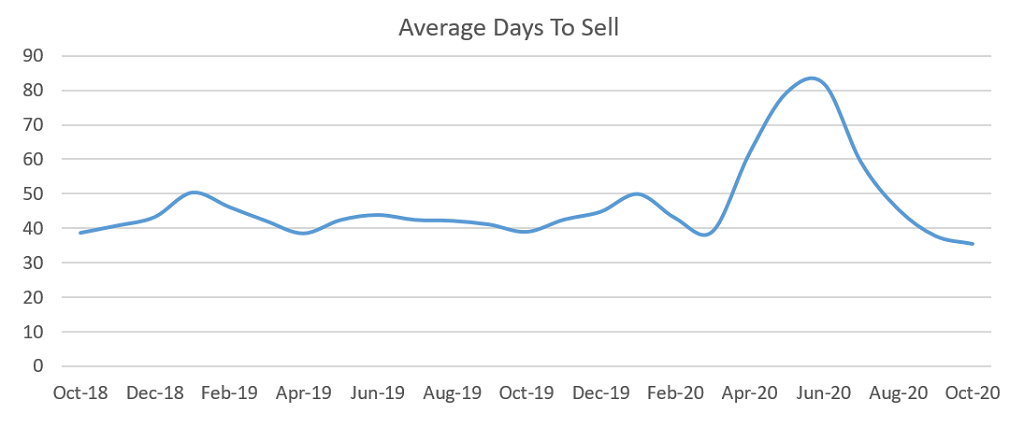

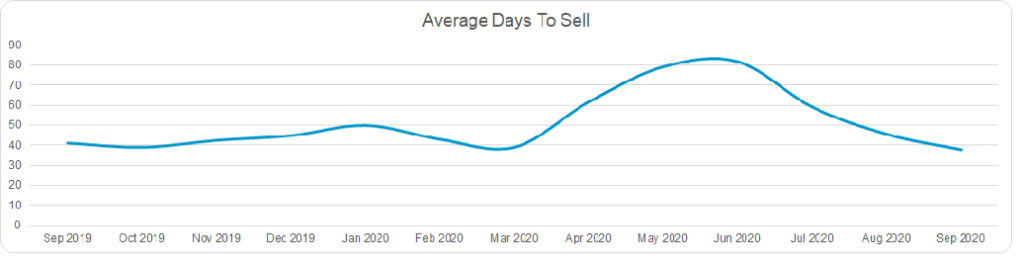

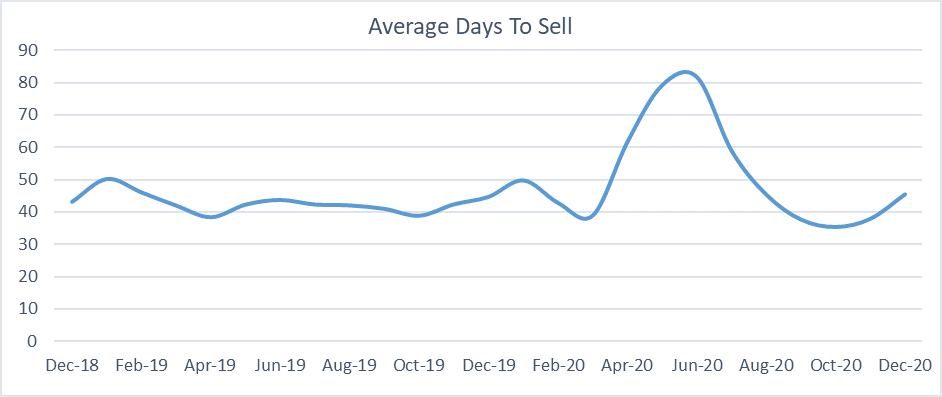

Glass’s Live Retail pricing tool measures the length of time a car spends on the forecourt. This is a useful barometer of the state of the used car retail market – the days to sell are lower when there is good demand and higher when times are tougher.

The average in December was 45.5 days to sell. This was 7.6 days longer than in November, but only 0.8 days longer than in December 2019, so in keeping with the time of the year. To achieve these sales, the average discount required was also higher in December than in the previous month, up from 2.5% to 3.1%, but still favourable when compared to the 3.7% average discount for December 2019.

Used car sales outlook

With the UK once again in a state of lockdown, the UK’s used car market has got off to a subdued start. The rollout of the vaccination programme and the agreement of a Brexit deal will help promote a degree of positivity and should translate into a recovery of the markets, although this will not be truly apparent until the second quarter of the year.

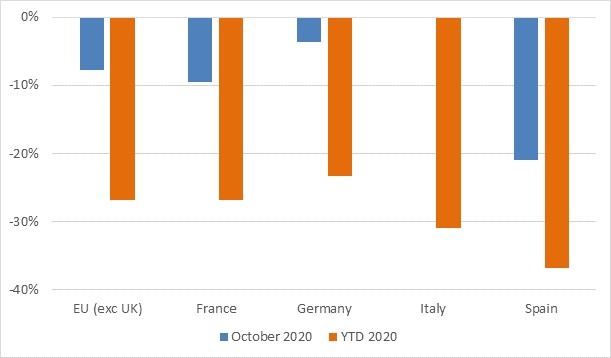

New car registrations were 29.4% down in 2020 from the total achieved in 2019 and whilst volumes will recover through 2021, registrations are unlikely to achieve “normal” levels this year. There are concerns that the significant reduction of registrations in 2020 will decrease the supply of sub 24-month-old “nearly new” vehicles, particularly diesel-powered cars. This concern is illustrated by the 2020 market share for diesel. The diesel market share decreased from 25.2% in 2019 to 16.0% in 2020 and equated to a 55% drop in volume. Petrol-power also saw large drops – although not to the same scale – which will also lead to a shortage of supply.

Alternative fuel vehicles

New car registrations in 2019 were primarily driven by availability rather than demand. Therefore the apparent swing towards alternative fuel should be viewed with a degree of caution. It is true to say that the market is undoubtedly moving away from pure ICE to alternative fuel vehicles, but 2020 was not a normal year and makes valid conclusions difficult to make. Indeed, 2021 may see supply distorted again, potentially in favour of ICE as manufacturers attempt to catch up on deliveries delayed from last year. However, with the increasing availability of PHEVs, HEVs and BEVs these powertrains will likely continue to take market share from traditional ICE variants over the coming months and years and continue to change the availability of fuel types at auction.

Moving forward, what can be said with a fair degree of certainty is that 2021 is going to be another “fascinating” year for both new and used car sales, with a much higher percentage of online sales than ever before.