Close

CloseMotorcycle registrations in January and February recorded growth over last year, suggesting the possibility of a positive year for 2020. Throughout this period, the threat of COVID-19 was present with many countries already going into lockdown. The full impact did not hit the UK until March 23 when Boris Johnson announced the lockdown, although the government had already encouraged social distancing.

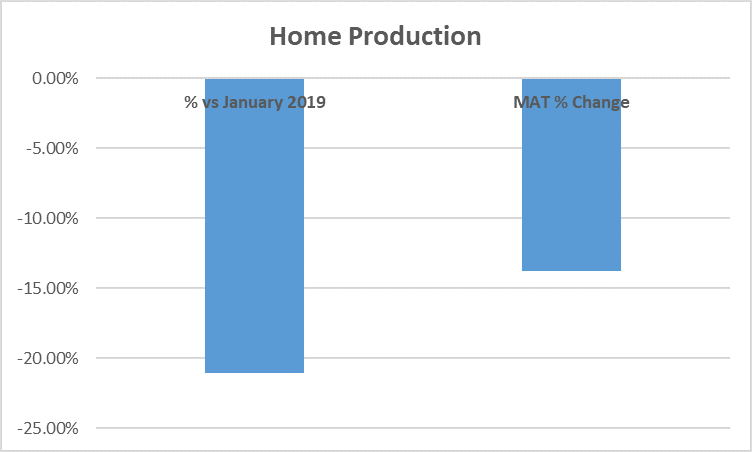

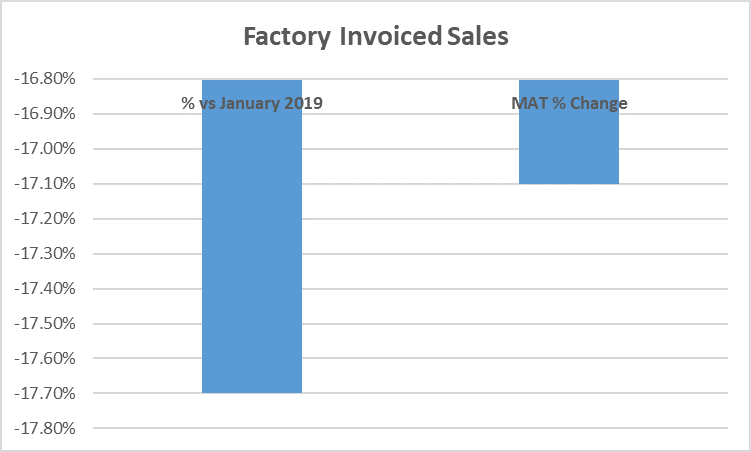

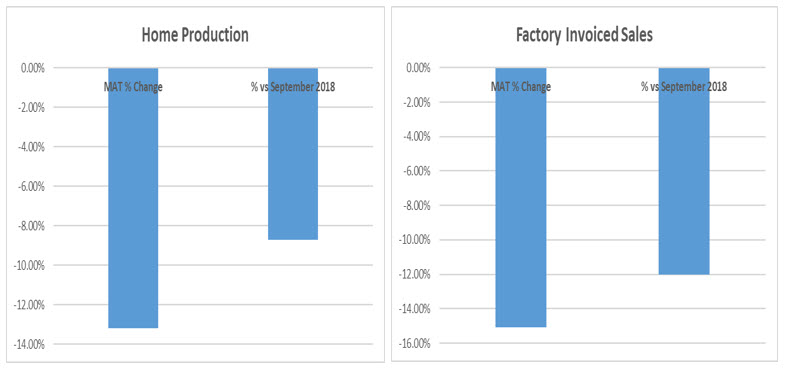

Unfortunately, it came as no surprise that the official Motorcycle Industry Association (MCIA) March registrations were 22% behind last year, with all style categories suffering a decline. Paul McDonald, Glass’s Leisure Vehicles Editor said, “After tentative signs that 2020 could be a stronger year for the industry, the spread of COVID-19 put pay to that during March. At the time of writing, the government has just extended the lockdown for a minimum of three weeks with no confirmation yet of an exit strategy”.

Prior to the lockdown on the 23rd, the dealer view of March was that demand was behind last year. Whilst some dealers enjoyed a reasonable start to the month, most agreed that with the growing uncertainty sales had gone quiet with some customers cancelling orders.

Hot YTD in March

- Honda PCX125 retains the top spot

- Yamaha NMax was runner up

- BMW R1250 GS performs strongly

- Royal Enfield value for money Interceptor 650 remains buoyant

What can the industry expect moving forward?

The world is experiencing unprecedented times, so it is impossible to accurately predict what this means for the industry in the near future. What is likely is that uncertainty will hinder consumer confidence for the rest of the year. At this stage, Glass’s view is that the industry will not grow this year.

Used Sales

Following good used sales numbers in February, dealer expectation for March to produce strong trading conditions was high. Speaking to dealers in the lead up to the March 23when showrooms closed, most held the view that March started with buoyant sales up to the 21st, although a few dealers had already experienced disruption to normal sales activities.

Top Selling Models

Many dealers reported a broad range of machines selling well, providing correct price and condition. The first shoots of increasing spring demand encouraged certain models to sell even those that had hung around through the winter.

- Ducati Multistrada

- Yamaha MT range

- Kawasaki Z900RS

- Triumph Bonneville

Stock

Stock availability was reported to be broadly in line with last year. Difficulties finding quality machines remain, compounded by fewer registrations in March, resulting in fewer part exchanges. However, in view of the current situation, most dealers will be sourcing less stock at the moment.

Sales Environment

When speaking to dealers in mid-March, there was understandably a degree of uncertainty regarding sales performance moving forward. As with the new market, it is impossible to forecast when sales and demand are likely to show signs of recovery. However, it is certain that the next few months are going to be tough with a good chance the used market will also be affected for much of this year and into 2021.

In May’s edition of Glass’s data, the 2069 plates have been added. After careful consideration taking into account the current situation, the majority of values have been reduced slightly except where trade feedback or evidence from the market place suggests further adjustments where necessary.