Close

CloseThe automotive retail sector began emerging from lockdown on 1 June with dealerships in England able to reopen showrooms, following strict social distancing measures. Many expected registrations to return to a degree of normality, however, it is worth remembering that non-essential retail sites in Northern Ireland, including dealerships, were unable to reopen until 8 June, with Wales following on 22 June and Scotland having to wait until 29 June. According to the Society of Motor Manufacturers and traders (SMMT), registrations in June 2020 were 34.9% lower than 2019 at 145,377.

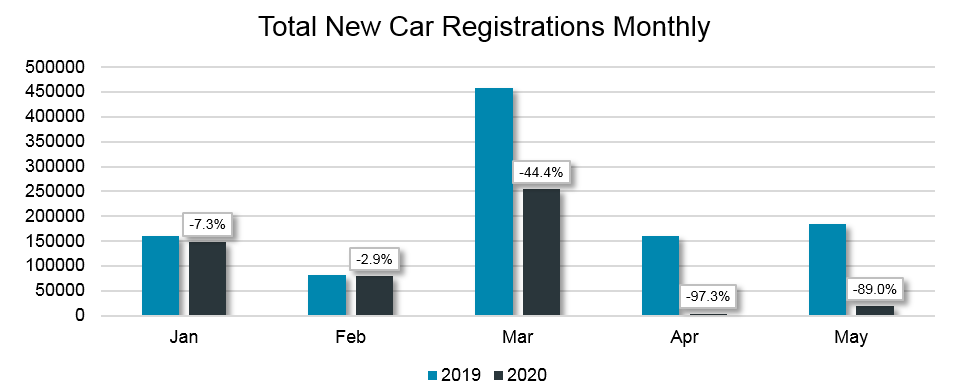

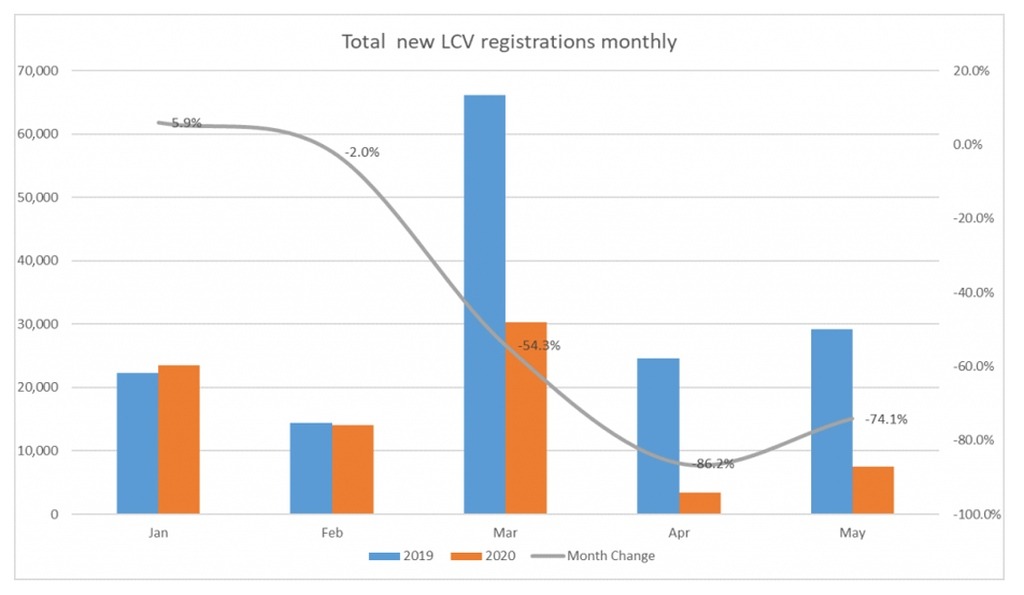

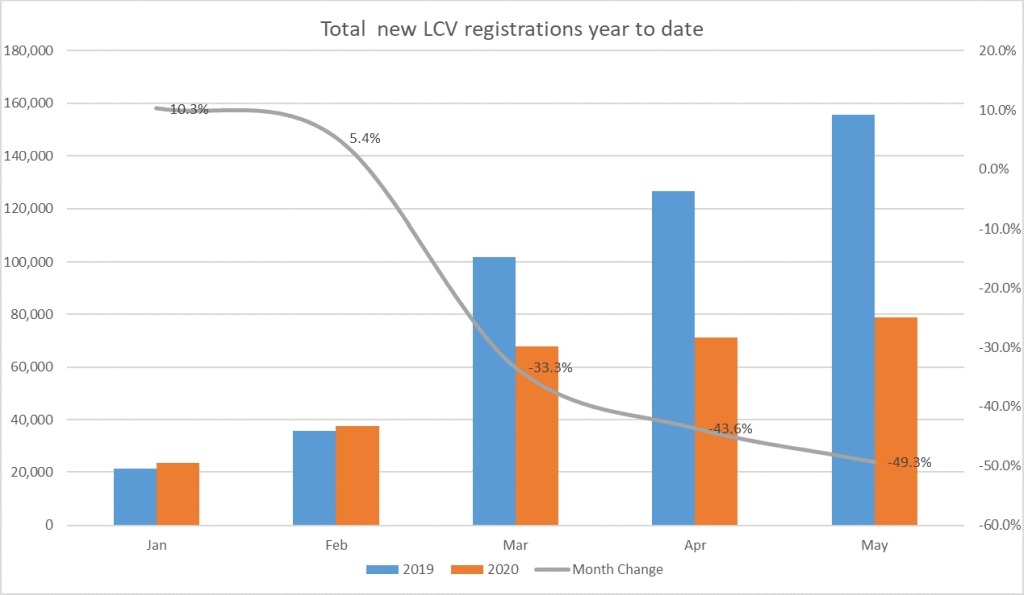

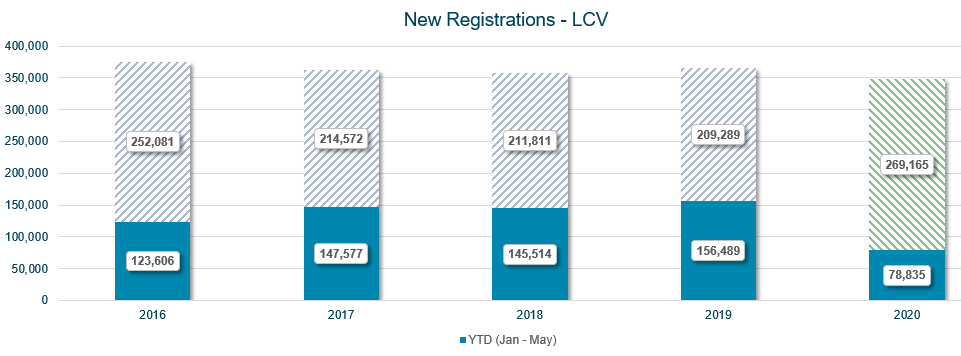

The new car market has been badly affected by the coronavirus related lockdown, and so far this year sits 48.5% lower than last year. Add to that, factory shut-downs and logistical delays around the world and the outlook for the new car market remains bleak. That said, the market also faltered prior to lockdown in January and February, being down 7.3% and 2.9% respectively. March’s registration tally finished down 44.4% on prior year, although the lockdown only knocked nine days of trading off the month, indicating that the new car market was already in trouble, although it is possible that the global coronavirus situation had already impacted supply and consumer confidence.

April’s registration total was 97.3% down on a year earlier, with May improving slightly with the help of ‘click and collect’ services, but was still down 89%. It will be interesting to see how the new car market will perform in July, with all dealerships across the UK trading throughout the month.

Used market

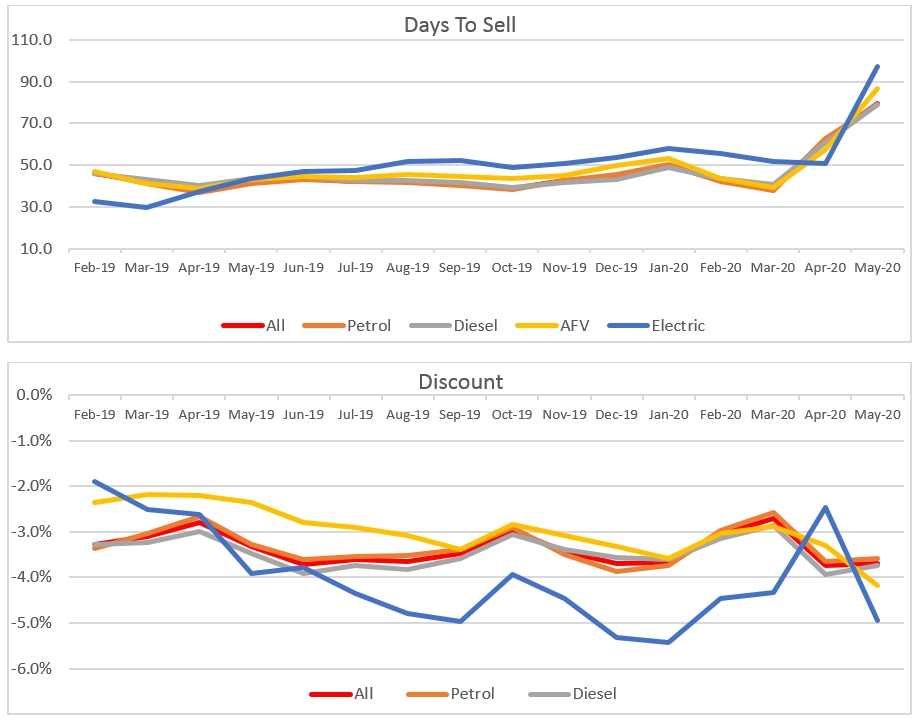

The volume of used cars selling through auction channels ramped-up in June, although overall sale volumes are still lower than normally expected at this time of year. Currently down around 10%, a combination of logistical issues, together with fewer part-exchanges coming from dealer groups due to the poor new car market performance, rather than a lack of demand.

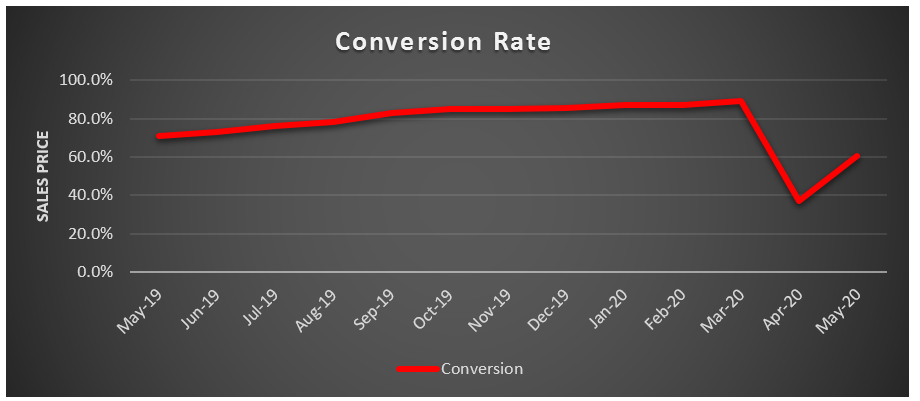

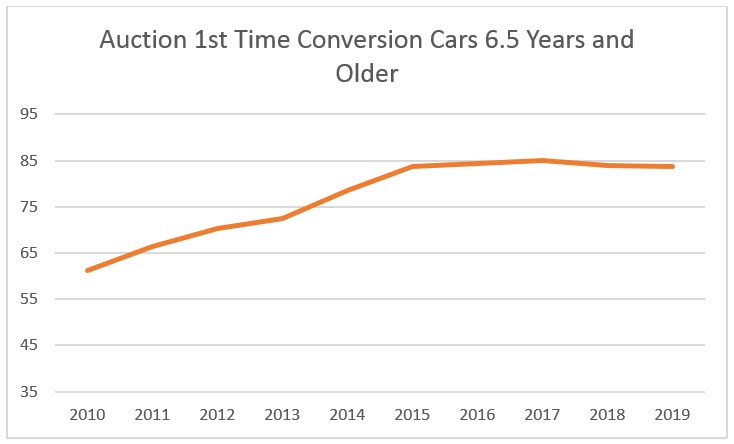

Activity strengthened in June helped by the reopening of retail sites in England, with an average first-time conversion rate of 81%. This is very strong for the time of year, no doubt boosted by pent-up demand in the market. June’s first-time conversion rate was almost eight percentage points better than June 2019, although still not in line with the exceptional performance seen just prior to lockdown in March, where 89% of stock sold at the first time of asking, driven by strong demand and a lack of used car stock entering auction channels.

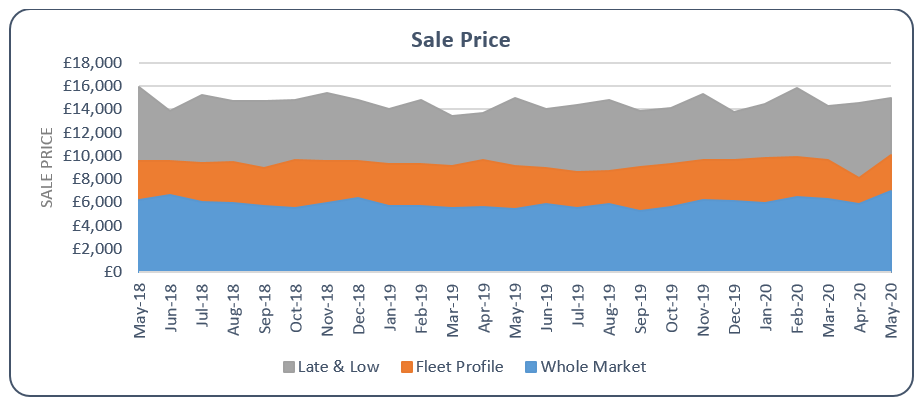

Now that demand has returned to the wholesale market, auction hammer prices have strengthened. When compared retrospectively with Glass’s Trade values in June, they were within 0.9%.