Close

CloseNew car sales

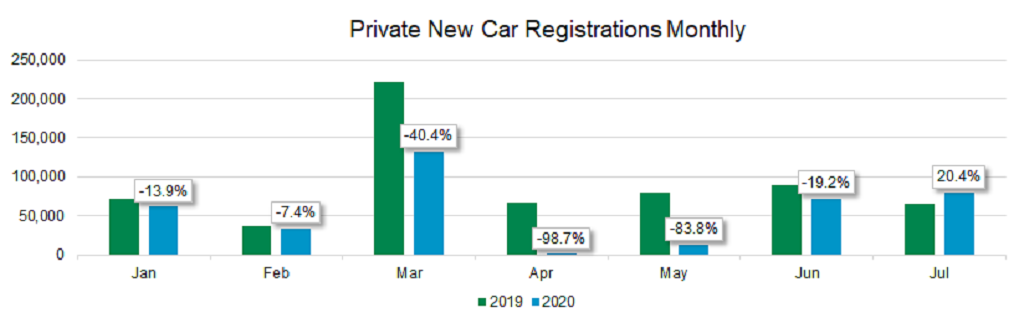

Manufacturers and dealers will take some comfort from the latest new car registration statistics from the Society of Motor Manufacturers and Traders (SMMT). Following a full month of trading across the UK, the new car market produced the first monthly positive result this year, being 11.3% up on July 2019, with pent-up demand finally materialising in registration numbers.

As July is not a high volume registration month, the increase has done little to impact the overall year-to-date position with the market sitting 41.9% lower than 2019 at just over 828,000 units. However, July’s result will give dealers and manufacturers some confidence that demand remains for new cars. With some attractive deals currently on offer, August should be similarly positive. However, the high-volume September plate change is the focus month for the industry, where delivering an increase versus September 2019 may prove difficult.

Used market

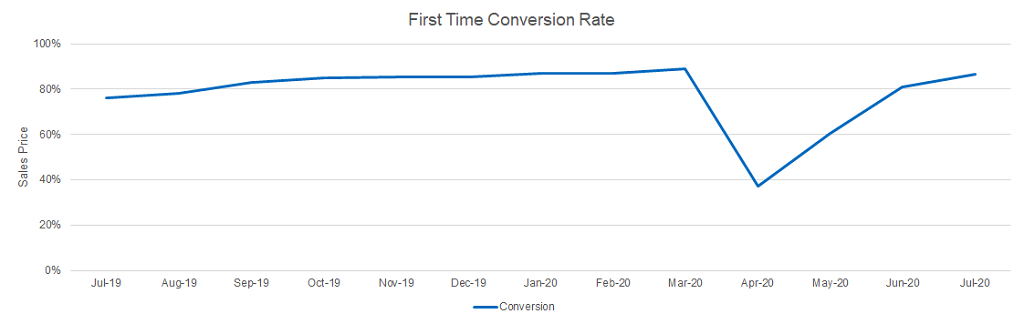

With some auction providers reporting higher stock levels than last year and an increase of over 10 percentage points in the first-time conversion rate to 86.4%, it underlines the buoyancy of July’s auction market. Hammer prices were also strong, exceeding Glass’s Trade values by 3.3% on average, leading to an increase in Glass’s values in August. With auction activity and hammer prices showing signs of further growth through August, the expectation is further increases in values in September, bucking seasonal trends.

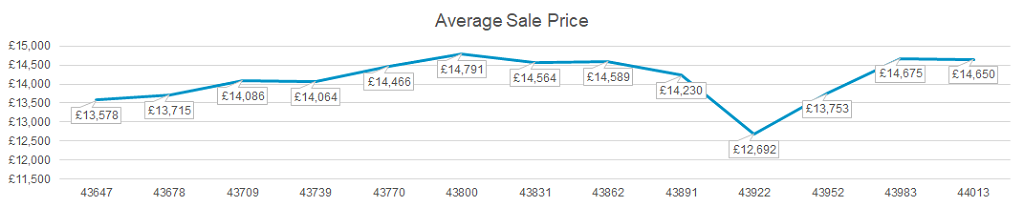

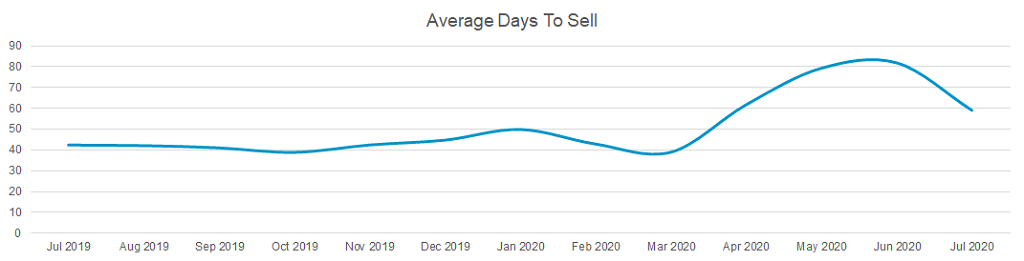

A strong retail market is driving this exceptional wholesale activity. In July the average days it took a dealer to sell a used car fell from 82 to 59 days according to Glass’s Live Retail pricing tool, rapidly returning to pre-lockdown levels (39 days in March) as fresh stock is added to forecourts.