Close

CloseFeatures on demand (FOD) can open up a world of potential, but not without risk. Sonja Nehls, principal analyst at Autovista24 explores the hot topic.

At the start of July, BMW quietly introduced heated seats as a subscription item to its ConnectedDrive store in several markets. The news sparked an intense debate online, with social media comments ranging from amused to worried.

BMW is in the hot seat, but the topic of FOD is a high-ranking one for all carmakers. Some are more advanced in the process, while others lag behind. Although getting the set-up of FOD right holds certain risks, both on the new and used-car market, there are major opportunities and potential benefits for all stakeholders.

FOD builds on over-the-air update (OTA) technology in a vehicle’s software and adds a commercial angle to it. Through FOD, customers can enhance their car’s set-up and activate certain functionalities for a trial, a limited subscription period, or the lifetime of the vehicle. In a recent video, Autovista24 deputy editor Tom Geggus explains what FOD is all about.

Advantages and opportunities for stakeholders include:

- Carmakers can simplify their production processes by unifying the hardware set-up of vehicles. The FOD platform represents a direct customer relationship and a potential revenue stream throughout the lifecycle of a car.

- Drivers can experience new features they did not initially order, enhancing and personalising their cars.

- Used cars with FOD capabilities can be upgraded individually and therefore appeal to a wider group of potential buyers. Remarketers benefit from increased flexibility and avoid take-it-or-leave-it scenarios.

- Fleets do their maths, taking into account the holding period of the car, costs for a FOD subscription compared to the lifetime buy, and implications on remarketing potential.

Not all items qualify for features on demand

Besides the reasonable advantages and opportunities, features on demand face challenges as to the right applications and cost, as well as how to ensure profitability.

Jennifer Bilatscheck, head of Car To Market and consulting at Autovista Group, has worked with a number of carmakers on consulting studies regarding FOD, and identified the main strategic challenges. ‘Selecting the right features at the right subscription price is key. Prices need to be high enough to compensate for the initial hardware investment and attractive enough to secure high take rates. If set up incorrectly, FOD could result in financial loss and impact residual values (RVs) negatively,’ she said.

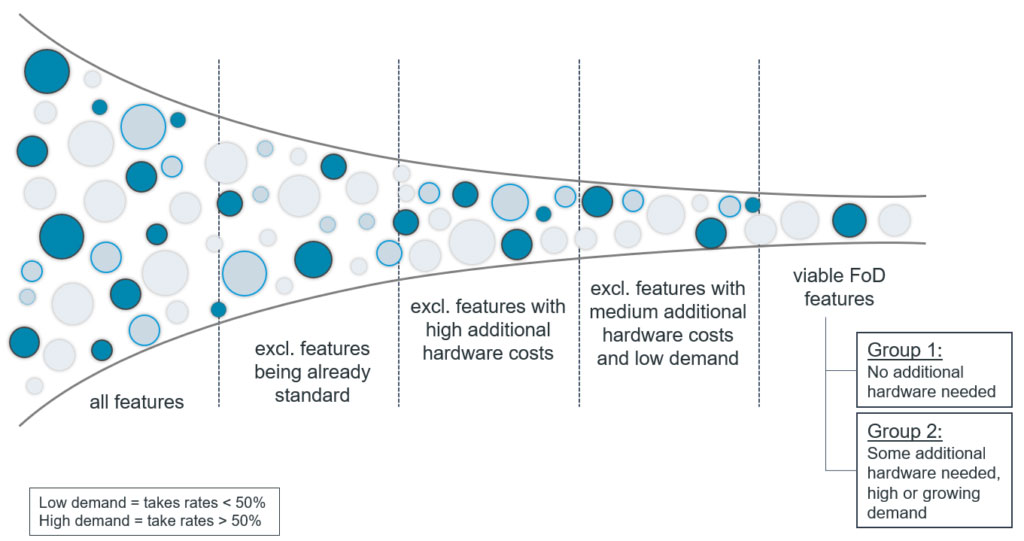

The team has developed a framework to identify eligible and commercially viable items for FOD, which on the one hand considers the desirability of a feature, represented by the take rate. On the other hand, it reflects the initial hardware investment needed to enable FOD for an item. Functions are commercially viable when there is no additional hardware needed or when the additional hardware is compensated for by a high or growing demand.

Viability of FOD depends on demand and hardware investment

In a recent Autovista24 webinar, Bilatscheck used an example now in the spotlight, heated seats, to explain the risks of FOD. ‘You cannot simply remove an item, which typically is a standard feature with the carmaker’s models, and then offer it as FOD. The basic RV would suffer and the FOD’s potential positive contribution to RVs will not outweigh that impact,’ Bilatscheck explained.

Also, the potential positive impact of the FOD capability depends heavily on the attractiveness of the FOD offer on the used-car market. Used-car buyers are more price-sensitive than new-car buyers.

If FODs are perceived as too expensive, the take rates in the later stages of the lifecycle, and therefore the contribution against initial hardware costs, will be very low and the RV impact of the capacity can even turn into a negative one.

Used-car buyers will deduct the required investment for activating the features they want from the price they are willing to pay for the car. A downward adjustment of prices in line with the overall depreciation of the vehicle will secure relevance for the second or third-hand owner.

Pitfalls for features on demand

The recent criticism BMW faced after it revealed heated seats as a FOD, showed that customers felt robbed of a feature which is already built into cars, but requires additional payment.

BMW UK shared a comment on this saying that ‘where heated seats, or any feature available in the ConnectedDrive store have been purchased when a customer vehicle is ordered, no subsequent subscription or payment is necessary.’ Additionally, there will now be the possibility to enable the heated seats at a later date, for the entire lifetime with a one-time payment of £200 (€235), or a more flexible monthly rate of £15.

In any case, the recent discussion showed that not all items are equally fit for FOD. There is a thin line between offering customers flexibility and putting them off.

FOD has major potential for all software-based functions, which can be truly enhanced and potentially add new features over the lifecycle, including advanced driver-assistance systems (ADAS) or navigation functions. Purely hardware-based items, like the heated seats, struggle with customer acceptance.

In May 2021, Sonja Nehls and Dr Christof Engelskirchen, chief economist at Autovista Group, touched on this in an Autovista24 podcast on the benefits and challenges of FOD. ‘A customer will know that everything is already built in and will assess the value of activating a feature lower than what OEMs hope’, Nehls said.

The podcast named the biggest pitfalls to avoid when it comes to FODs and the used-car market:

- Transparency of activated features and available FODs is crucial to find eligible vehicles and identify the equipment level, especially in comparison to conventionally-equipped cars.

- Off-lease vehicles will lack some important features due to expired subscription periods. Attractive packages targeting used-car buyers are needed to mitigate an RV risk for these vehicles.

- A clear definition and process are still needed as to taxation and benefit-in-kind for company-car drivers.

Features on demand come with opportunities and challenges. The advantages, especially for remarketing, are promising and enable more flexibility. Carmakers benefit from streamlined production processes, a direct customer relationship, and potential revenue streams.

The current debate on heated seats makes it crystal clear that not all features are eligible and that transparent communication with customers is key, regardless of whether a new or used car is being sold.