Close

Close

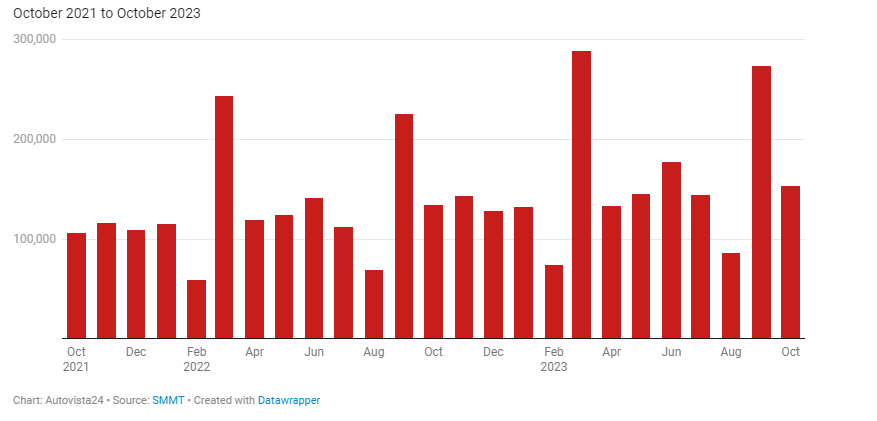

The UK’s new-car registration figures in October beat 2019’s numbers for the first time since the COVID-19 pandemic struck, highlighting the strength of the country’s automotive market recovery.

Last month, registrations in the UK were up 14.3% year on year, with the latest figures from the Society of Motor Manufacturers and Traders (SMMT) showing 153,529 new cars took to the country’s roads. This was also 7.2% up on October 2019, with 10,251 more units than four years ago.

This is the first time new-car registration data has improved on pre-COVID-19 pandemic figures, with 2019 held as the benchmark that the market needs to beat to show a return to form. Since then, there have been a number of challenges affecting new-car uptake.

This includes the pandemic itself and associated lockdowns, a supply-chain crisis that impeded vehicle production and deliveries, and economic instability which has hit household and business budgets.

UK new-car registrations

A deeper dive into the SMMT figures shows that large fleets were accountable for last month’s growth, while the private battery-electric vehicle (BEV) market continued to struggle, despite investment in public charging infrastructure.

Fleets forward

The fleet market has driven the UK’s registration figures into a 15th consecutive month of growth and has much to do with the rise in figures across the year.

October marks the 13th month in a row that fleet registrations have outperformed those of private deliveries. Last year’s figures swung heavily in the consumer’s favour, leading the market for eight months in total. Yet since delivery backlogs started clearing, large businesses have been driving the country’s automotive market.

Last month, fleet registrations were up 28.8% compared to October 2022. This means 87,479 cars took to the road thanks to large businesses, accounting for 57% of the market. Private sales, however, were stable, with a small 0.3% increase, equating to 62,915 units (41% share), just 177 more than last year.

Smaller business figures declined by 15.2% in October. However, this sector only makes up a small portion of the UK’s overall registration data, and while a double-digit drop looks severe, it equates to just 560 units overall, with 3,135 registrations last month making up 2% of the overall market.

The significance of fleet domination can be seen in the year-to-date figures. In the first 10 months of 2023, the overall UK market is up by 19.6%, with 1,605,437 registrations. 53.2% of this went to the fleet sector, up from 45.2% in the first 10 months of 2022, with 854,372 units equating to a growth of 40.8%.

Meanwhile, private registrations went up by just 1.6%, with 713,301 cars making up 44.4% of the market. This is down from 52.3% in the first 10 months of 2022. Small business registrations increased 11.2% to 37,764 units in the year to date, with a stable market share of 2.4%, from 2.5% this time last year.

Private BEV registrations struggle

The fleet sector is not just responsible for the UK’s new-car registration growth in 2023, but also the impressive uptake in BEVs, with the private sector struggling to adopt the zero-emission technology.

BEV uptake increased for the 42nd month in a row during October, with a 20.1% rise in the month working out to 23,943 units. The technology took a 15.6% market share, however, this is only up from 14.8% across the same period in 2022. Year-to-date figures were more positive, with 34.2% growth across the first 10 months of 2023, meaning the powertrain technology holds 16.3% of the market so far this year.

However, of the 262,487 BEVs registered in 2023, only 62,478 were private. This means only 23.8% of BEV deliveries took place outside the fleet and small-business market, suggesting a struggle to get consumers engaging with all-electric vehicles.

Plug-in hybrid (PHEV) registrations improved in October, with the 14,285 deliveries up 60.5% on the same month last year, with 9.3% of the market, up from 6.6% in October 2022. This means the entire plug-in market took 24.9% of the new-car market in the month.

Disproportionate infrastructure growth

The performance of plug-in models follows a significant increase in the UK’s charge point rollout during the third quarter of 2023. According to SMMT data, 4,753 new standard points, the largest ever quarterly total, came online between July and September.

This equates to one new public location for every 26 plug-in vehicles taking to the roads in the same period. This was an improvement from the one to 38 ratio during the same period last year.

However, installation was disproportionately focused on London and the south-east, which received four out of five new charge points commissioned during the quarter, despite the region accounting for fewer than two in five new plug-in registrations during the same period. In comparison, just 13 chargers were installed in Yorkshire and Humberside, while the north saw 105 chargers taken out of service.

This uneven distribution could impact private BEV registrations in particular, with many potential buyers likely to rely on the public infrastructure, especially those without access to off-street parking.

The SMMT is calling for binding targets for charge point rollout, in line with those set for the automotive market by the Zero Emission Vehicle Mandate. This would also need to be supported by the necessary changes to planning and grid connections, which would also help accelerate installations.

Unlike other major European markets, the UK has no incentive scheme in place for BEV purchases. This is likely impacting private sales, with vehicles still prohibitively expensive for some.

The overall performance is in line with other markets, but the needs of businesses to build their environmental credentials, rather than the willingness of the public to adopt zero-emission technology, seems to be the main driver.

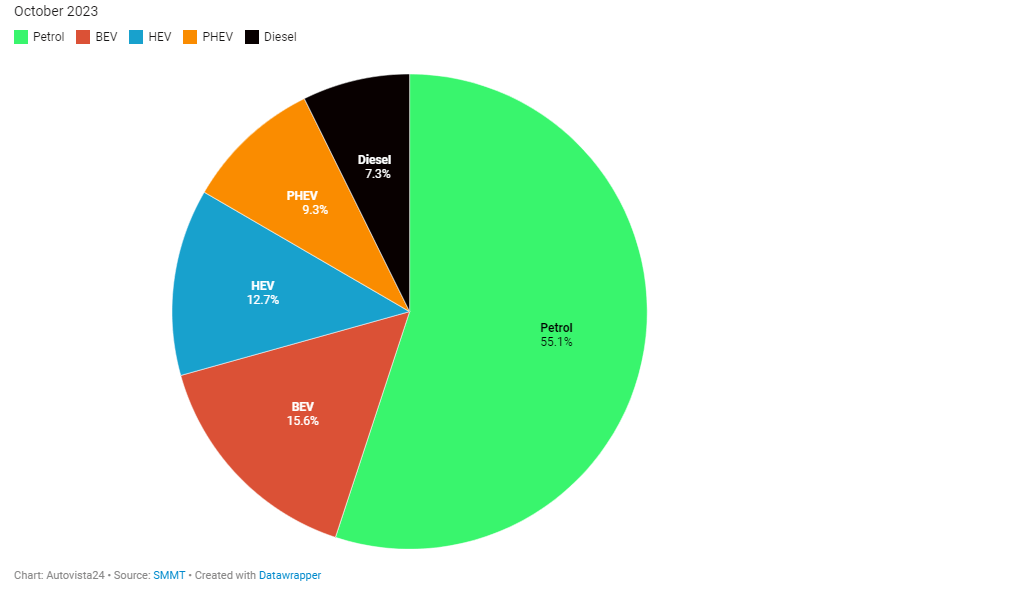

Petrol leads the market

The poor performance of the private sector does not take away from the fact that BEVs were the second most popular powertrain in the UK last month. The strong fleet uptake will also translate into the second-hand segment in three years, as these businesses de-fleet. This will give private buyers who cannot afford a new model the opportunity to experience zero-emission motoring.

UK new-car market share by fuel type

Petrol once again led the registration figures last month, with 84,451 units, including petrol mild hybrids (MHEVs). This was an improvement of 8.3% against last year, however, the market share of the fuel slipped to 55% from 58% in the previous period.

Diesel suffered another month of losses, with 11,276 units, including MHEVs, equating to a 4.5% fall. With just a 7.3% market share, the fuel dropped to the bottom of the chart in October.

In the year-to-date numbers, petrol-powered cars increased their registrations tally by 17.4%, with a market share of 56.4%, down from 57.4% at the same point last year. Diesel saw deliveries drop 9.4% in the first 10 months, with a 7.6% market share. However, this is above the share for PHEVs with 7.1% of the new-car market.

Hybrids saw a 24.4% improvement in the month, with their 19,547 deliveries holding 12.7% of the market. So far in 2023, hybrid registrations are up by 27.8%, placing them firmly in third place amongst the fuel types.

SMMT downgrades BEV outlook

The SMMT has revised its market outlook upwards to reflect the better-than-expected market growth. Overall new-car registrations are anticipated to reach 1.886 million by the end of the year, a rise of 2.1% from July’s expectations. However, forecasted BEV uptake was downgraded again slightly, by 1.7% to 324,000 units, resulting in an expected overall 2023 market share of 17.2%.

Looking ahead to 2024, the overall market outlook is marginally more positive, up 1% to 1.97 million units, a 4.4% rise on the 2023 outlook. With an absence of consumer incentives and an overwhelming dependency on fleet registrations for growth, the BEV market share outlook has been revised downwards to 22.3%, despite 439,000 expected registrations, a 35.5% increase on 2023.

This content is brought to you by Autovista24.