Close

Close

Residual values (RVs) held steady in July across European used-car markets. Trade RVs presented as a percentage of the original list price (%RV) saw only marginal deviations for 36-month-old cars at 60,000km.

The UK experienced the greatest month-on-month decrease. A 2.1% drop left the country’s %RV level at 62.6%. Meanwhile, France saw the largest %RV upswing, with its values increasing 0.7%, reaching 56.3%.

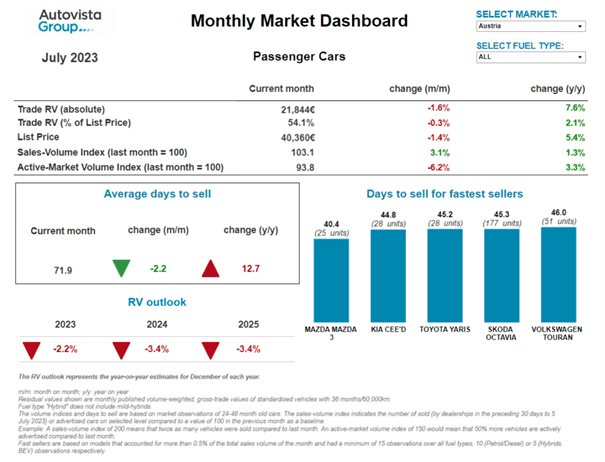

The country also saw the greatest increase in absolute residual values, up 2.3% compared with June. This puts the average trade value for a 36-month-old car in France at €19,700, up from €19,235 in the previous month. Austria experienced one of the largest value declines, with prices moving from €22,205 in June to €21,844 in July (down 1.3%).

While many European markets saw used cars sell more rapidly in June, this slowed significantly in certain countries during July. After a month-on-month decline of 14.4 days in June, the speed of sales in Italy increased by 17.2 days last month. The second greatest increase occurred in Spain, where used cars spent an additional 9.8 days on the forecourt.

Used cars only sold faster in Austria and Switzerland, taking 2.2 and 0.8 fewer days to sell respectively than in June. For Austria, this is the second consecutive month of faster sales, taking the total in July down to 71.9 days. But this was the first time this year Switzerland was able to reverse its trend of slowing sales, now standing at 80.4 days.

Month-on-month changes in the sales volume index (SVI) and active-market volume index (AMVI) reveal that most markets saw a great upswing in demand than supply in July. Switzerland experienced the greatest SVI increase of 20.2% compared to June, while the AMVI fell by 2.2%. The only exception was Italy, where a 24.9% decline in demand was overshadowed by a 0.8% uptick in supply.

Click here to open the interactive dashboard

The interactive monthly market dashboard examines Austria, France, Germany, Italy, Spain, Switzerland, and the UK. It includes a breakdown of key performance indicators by fuel type, including RVs, new-car list prices, selling days, sales volume and active-market volume indices.

Demand slowing in Austria

Living costs in Austria have climbed continually this year when compared with 2022. However, the sales volume index revealed stronger demand in July, with month-on-month growth of 3.1% and a year-on-year increase of 1.3%. The month also saw a 3.3% year-on-year improvement in the supply volume of two-to-four-year-old cars. But it is worth recognising that supply was markedly lower in 2022 when compared with the pre-COVID-19 period.

The average number of days it took to sell a used car decreased to 71.9 in July, after strong increases in the first half of the year. Overall, this development confirms a slowdown in demand. Hybrid-electric vehicles (HEVs) sold the fastest in the month, averaging around 56 days, followed by diesel cars with 70 days, petrol cars with 71 days and plug-in hybrids (PHEVs) at around 82 days. Battery-electric vehicles (BEVs) sold more slowly, around 94 days.

‘As demand weakened and supply improved, %RVs of 36-month-old cars decreased slightly by 0.3% compared to June, reaching an average of 54.1%. This marks a 2.1% year-on-year gain but shows that pressure on RVs is increasing,’ said Robert Madas, Eurotax (part of Autovista Group) regional head of valuations, Austria, Switzerland, and Poland.

HEVs boasted the largest %RV trade value of 57.9% followed by PHEVs (53.4%), diesel cars (54.3%) and petrol cars (55.1%). BEVs retained the lowest value at 47.7%. Mounting pressure on RVs can be expected as supply recovers and demand drops. So, RVs of 36-month-old cars are set to stay relatively high, while following a decreasing trend.

‘The average %RV of a 36-month-old car at 60,000km is projected to end this year roughly 2.4% down on December 2022. As for next year, %RVs are expected to drop by around 3.4% year on year due to growing supply and shrinking demand,’ Madas added.

Positive developments for France

Compared with June, France saw a slight increase in absolute RVs last month, with list prices also growing. Sales volumes saw the most positive month-on-month developments, following continual declines so far in the year. However, this demand is still down significantly compared with 2022.

The fastest-selling cars were still the cheapest and smallest models. The Dacia Sandero sold the fastest after an average of roughly 31 days, followed by two Toyotas, the Yaris and the Aygo. As previously forecast, budgets are influencing purchasing decisions, pushing consumers to lower segments.

Petrol and diesel models were effectively on par with the overall market trend. The RVs of diesel-driven cars held firm, even with their tarnished reputation and the implementation of low-emission zones (ZFEs) in the country.

Only cities with 150,000 inhabitants or more, are currently impacted by ZFEs and high-milage drivers are not affected at all. However, from late 2024 and into 2025, diesel will feel the effects more heavily, particularly with the ‘Crit’Air Sticker 2’ coming into play in Paris.

Compared with June, HEV RVs increased, both in absolute and %RV terms, alongside sales volumes. PHEVs saw stable RVs, with even greater growth in the sales volume index thanks to greater availability on the used-car market, as well as improved ranges. Absolute RVs of BEVs fell slightly month on month, due to dropping list prices. Sales volumes increased as these all-electric models become more affordable.

‘Even with a higher level of sales overall, the market has still not recovered, even falling short of last year’s performance. Sales are still being driven by budgets, pushing purchases into lower segments. Older cars will suffer the least from this market trend,’ said Ludovic Percier, Autovista Group residual value and market analyst for France.

The party is over in Germany

‘When it comes to the used-car market, the consensus within the automotive industry appears to be that the party is over. Stock volumes and average days to sell are growing once again, while prices are coming under increasing pressure,’ commented Andreas Geilenbruegge, head of valuations and insights at Schwacke (part of Autovista Group).

The growing share of electric vehicles (EVs), including PHEVs and BEVs, is causing problems due to a lack of sufficient demand in the German used-car market. However, the situation does not seem quite so dire when contrasted against more difficult periods, such as during the COVID-19 pandemic. In this comparison, current key performance indicators such as average prices, %RVs and even days in stock, are still advantageous on average.

The growing gap between increasing supply and weak demand is causing problems. Compared with the first half of 2022, more used vehicles were sold between January and June this year, but stock levels are climbing much faster than sales. Moreover, BEVs and PHEVs now account for almost 15% of newer used-car stock, which is a rapidly accelerating trend. The issue is that too few buyers are seeking out these models.

Supply for the coming years has become quite stable again too. Fleet registrations are seeing a record year, with large fleets making a significant contribution. However, this uptake consists of an increasing percentage of electrified models.

‘There is hope that tactical registrations from the likes of dealers, manufacturers and rental companies have not yet been returned to the level of earlier years. These vehicles usually reach the used-car market six to 18 months after initial registration. This means less pressure on the used-car market and its prices,’ Geilenbruegge added.

However, internal-combustion engine models are under less pressure. They still represent the vast majority of the market and are mostly selling at stable prices. There is still a lack of enticing government-driven benefits for EVs. The ownership and operation of electric vehicles need to be made more appealing in order to stoke demand for used models.

Change is coming to Italy

‘It would be fair to say that the first half of 2023 has been a period of substantial stability for the Italian used-car market, with small variations in RVs,’ stated Marco Pasquetti, head of valuations, Autovista Group Italy. ‘However, operators in the sector have been warning for a few months that change is coming,’

July presented the first evidence of this emerging adjustment. Compared with June, there was a 1.2% drop in %RVs. This was the result of increasing list prices and decreasing absolute RVs. This drop in %RVs was recorded across all fuel types, with the sole exception of LPG vehicles, which instead saw a marginal growth of 0.4%.

Despite this overall downward trend, the market is still performing better than in July 2022, with average absolute RVs up 27.4%. This means that the average 36-month-old car is now worth €4,500 more than it was at the same point a year ago (not adjusted for inflation).

The time it took to sell a used car also increased in July, models remained in stock for an average of over 65 days, 17 days longer than in June. While stock levels of HEVs grew, these vehicles were also the fastest selling, taking fewer than 52 days on average to pass through a dealership. Meanwhile, natural gas vehicles and BEVs saw some of the slowest selling times, both above 70 days. However, it is worth recognising that the sales volume of both powertrain types is quite low.

Peak tourism season in Spain

The first half of the year closed with a near 25% increase in new-vehicle sales, still lower than pre-pandemic records but very close to expected market levels. The private channel remains restricted, with interest rates slowing purchasing decisions. Meanwhile, the corporate channel is growing steadily. The arrival of the peak tourism season has pushed the rental channel to achieve growth of 70% in the first half of the year, after more than a year of product drought.

‘On the other hand, the used-car market grew moderately by 2.7% in the first half of the year,’ commented Ana Azofra, Autovista Group head of valuations and insights, Spain. ‘Leasing companies continue to supply young used cars, and for the first time in recent years, sales of older models have slowed. However, despite this deceleration, these cars continue to best maintain their average transaction price.’

In contrast, the downward trend in the average transaction price of models up to six years old continues. For example, while the value of a three-year-old used car at 60,000km remains 5% above the levels seen in 2022, prices are beginning to drop slightly each month. This trend is more intense the younger the used car is.

Other market indicators, such as average days to sell a used car have also worsened. In July, this indicator increased by nearly 12 days for petrol vehicles, eight for diesel, seven for HEVs and almost six for PHEVs. Only BEVs saw an improvement, taking four fewer days to sell on average, despite their stock levels increasing by 50% month on month.

‘Reflecting current market trends, residual values are forecast to fall 1.8% by the end of this year, with less severe declines expected in 2024 and 2025,’ said Azofra.

Transactions slow in Switzerland

Switzerland’s active-market volume index was 2.2% lower month on month in July across all two-to-four-year-old passenger cars, but 33.4% higher than a year earlier. Used-car transactions have also slowed since the beginning of the year as costs of living soared.

The sales-volume index increased by 20.2% compared to June and is up 25.7% year on year. With increased supply and overall weakening demand in the last few months, the average %RV of a 36-month-old car decreased again. The figure fell to 50.5% in July, down 0.2% month on month, but still up 0.3% year on year.

HEVs posted a particularly strong year-on-year %RV gain of 11.1%, reaching a total of 54.5%. This was followed by petrol cars (51.5%), diesel models (48.7%) and BEVs (47.8%). 36-month-old PHEVs retained 47.8% of their original list price.

The average days to sell decreased in July, with a passenger car aged two-to-four years in stock for 80 days. HEVs sold the quickest after an average of 77 days, followed by petrol cars after 78 days, then diesel cars after 81 days, BEVs after 90 days, and finally, PHEVs after 92 days.

Hans-Peter Annen, head of valuations and insights, at Eurotax Switzerland, explained that used-car demand can be expected to weaken amid overall high and stable supply. ‘A further and slightly accelerated fall can be expected, although values of three-year-old used cars remain relatively high.’

The %RV is forecast to finish 2023 down roughly 4.2% on December 2022. In 2024, RVs are expected to fall by around 4% year on year due to constant supply and lower demand.’

Concerning depreciation in UK

The average trade %RV of a 36-month-old car fell from 64% in June to 62.6% in July, representing a typical level of depreciation that would be seen in a non-COVID-19-affected market. Meanwhile, the average number of days it took a dealer to sell a used car increased from 38.5 to 39.5, indicating that retail activity has begun to slow, as is usually the case in the summer months. However, certain models are still proving popular, selling at a much faster rate.

In what will be a surprise for some, the fastest-selling car was a BEV. The Tesla Model 3 took dealers an average of just 22 days to sell. It seems that following significant month-on-month market-driven depreciation, BEVs may have hit a price point that makes them appear reasonable to consumers as a value-for-money proposition.

‘The average %RV of a three-year-old BEV in the UK fell from 64.4% to just 44.2% over the course of 12 months. A depreciation of 20 percentage points is very concerning over such a short period,’ said Jayson Whittington, Glass’s (part of Autovista Group) chief editor, cars and leisure vehicles. ‘Many industry figures will be hoping that BEV values are now beginning to stabilise. But how do current BEV values compare with other European countries?’ he asked

This month’s dashboard shows that of the seven countries reviewed, the UK sits in fifth place. The UK’s average BEV value is 4.6 percentage points lower than the highest-performing country, Spain. However, this is still a better result than recorded in France and Italy, with the UK’s BEV RVs sitting on a broadly similar level to the average across the seven reviewed markets.

‘This should inspire some comfort, as BEVs may now have found a new level which is in line with other markets. While Glass’s expects BEV values to continue to depreciate in 2023, this should be at a similar rate to other fuel types,’ said Whittington concluded.

This content is brought to you by Autovista24.