Close

Close

The resilience of diesel

As we reach the halfway point in the year, we reflect on how the UK new and used car markets have developed together with a possible direction for the rest of the year and 2020.

June 2018

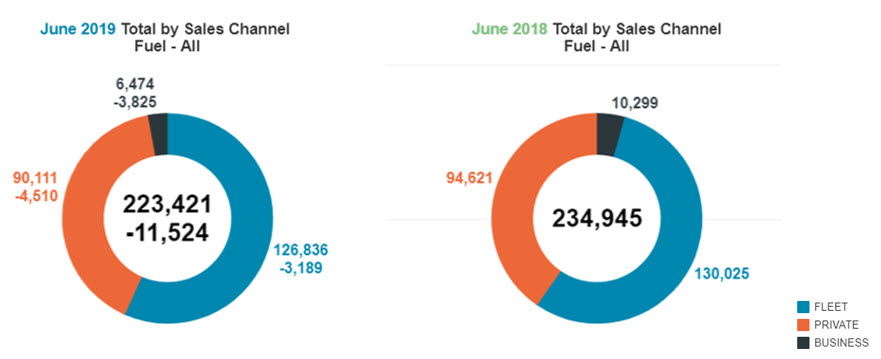

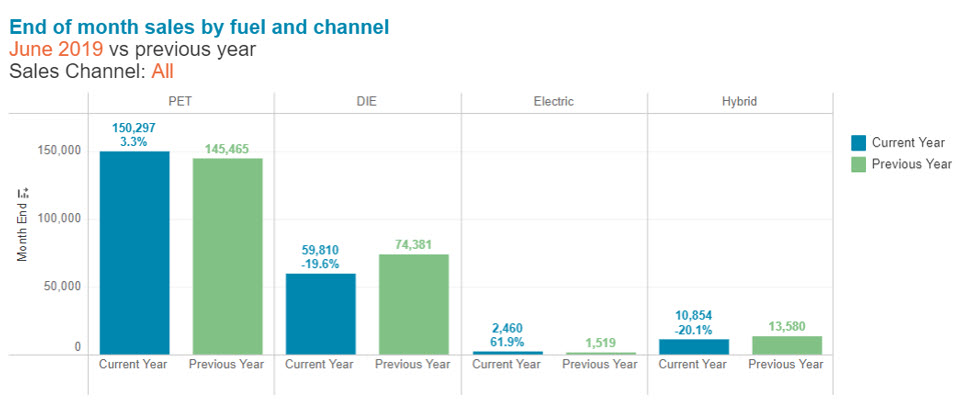

New car registrations fell again in June according to the UK’s Society of Motor Manufacturers and Traders (SMMT). Overall registrations fell by 4.9% versus June 2018 to 223,421 whilst diesel car registrations fell for the 27th consecutive month, by 20.5%, and show no sign of an imminent recovery.

Sales Channels

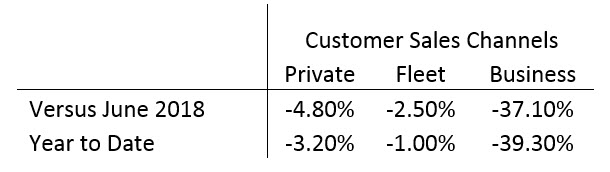

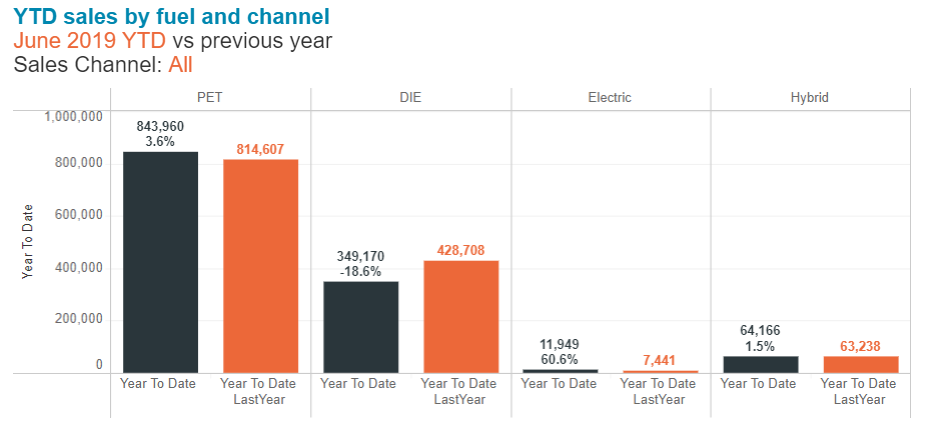

In the main sales channels, the story so far this year is negative however; the year-to-date comparison is a little brighter than the June 2018 to June 2019 comparison for private and fleet.

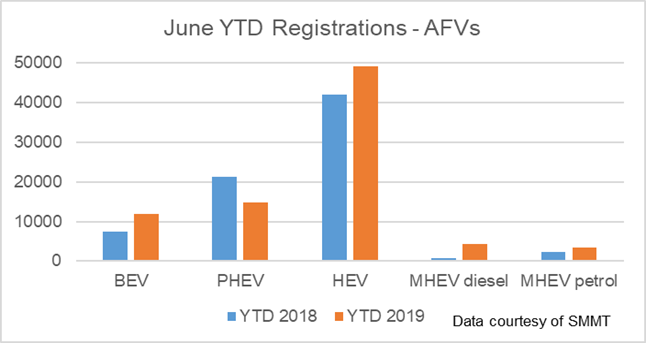

Surprisingly, an overall 4.3% negative trend for alternatively fuelled vehicles in June, driven by a 4.7% fall in demand for self-charging hybrids and an incredible decline of 50.4% for plug-in hybrids shows instability in the market. This decline is partly due to availability and partly due to the removal of the plugin grant by the UK Government. The SMMT’s Chief Executive Mike Hawes continues to raise concerns that the billions invested by manufacturers to bring these vehicles to market “are now being undermined by confusing policies and the premature removal of purchase incentives”. However, registrations of battery electric vehicles (BEV) grew substantially in percentage terms (up 61.9%). In reality, this large percentage increase only represents 941 units.

Petrol car registrations increased in June by 3.3% accounting for 66.9% of the market, an increase of over 5 percentage points compared to last year. The diesel share fell by 5 points to only 26.4% following the 27th consecutive monthly decline, in June being down 19.6%.

Year to Date 2019

With the exception of a small amount of growth in February, new car registrations have struggled throughout the first half of 2019. Brexit related economic and political uncertainty has contributed to an overall feeling of unease across most sectors including automotive and continues to influence the declining automotive market. However, the major factor appears to be the continued decline in diesel sales.

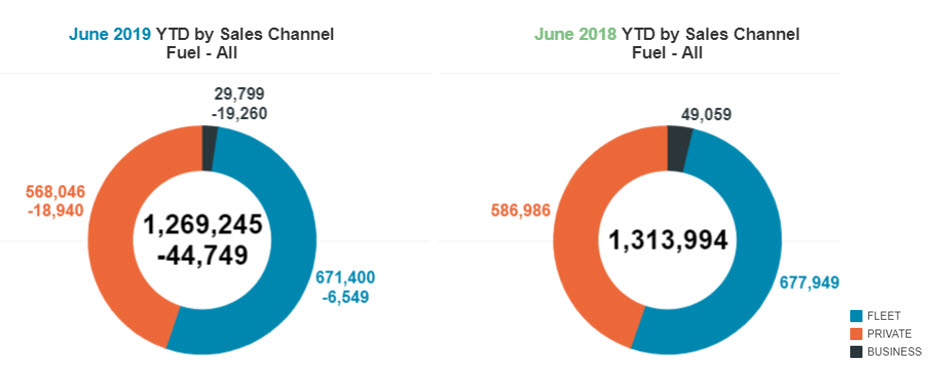

So far, in 2019 total new car registrations have fallen by 44,749. Solely analysing diesel registrations, sales of this fuel type are down an astonishing 83,129. The dramatic shift away from diesel began in 2017 when significant negative press reporting started having an effect on sales.

Last year, the introduction of WLTP testing also affected diesel take-up in the company car market, with drivers deferring taking a new car until they fully understood what revised CO2 figures would look like and how that would affect their benefit-in-kind (BIK) tax liability. There were also significant supply issues that led to leasing contract extensions. This year sees further complications. In September a new engine emissions standard comes into force (RDE2). New diesel cars that meet this standard will no longer attract the current diesel BIK penalty of an additional 4%. It is likely that company car users that are due to change will hold off choosing a new car until many more RDE2 compliant cars are available in the market.

So far, in the first half of 2019 new car registrations have fallen by 3.4% versus 2018 with the majority of the decline coming from the Private and Business sales channels.

In terms of the fuel type split, diesel continues to be the hardest hit fuel type with a year to date decline of 18.6%.

The SMMT’s June statistics set out the impact that mild hybrids are having on the new car market, for the first time. Mild hybrids are becoming increasingly popular with manufacturers adding them to their ranges. Depending on installation, they can allow internal combustion engines to be switched off whenever a car is coasting, braking or is stopped, and can restart the engine quickly when required. The mild hybrid element can also boost power output. Not designed to power a vehicle with battery alone, they do not need the same level of battery storage capacity as a full hybrid. Although, without this they are unable to achieve the fuel efficiency associated with a full hybrid, they still save drivers money at the pump and reduce CO2 emissions compared to pure internal combustion engine cars.

Year to date 2019, there have been 4,293 mild hybrid diesel cars registered compared to just 702 last year, a rise of 511%. As for petrol mild hybrids, there have been 1,212 more registrations than last year, a 52.4% increase. Although AFVs fell in June, their overall year-to-date position including mild hybrids remains strong, with growth of almost 14%. What is currently unclear is whether mild hybrids class as alternative fuel vehicles or not.

The used market

The UK wholesale auction market is showing some very small signs of recovery. While buyer activity is not yet back to the level it was last year, recent guide value reductions have started to make cars look better value for money, stimulating the market. However, the notoriously lack-lustre summer period is here with record UK temperature levels of 37 degrees, so a marked recovery is not expected. That said, with first time conversion rates two percentage points higher than in May, vendors should draw comfort that the downward trajectory the market experienced so far this year, is starting to level out.

In the UK retail used car market prices are taking longer to reduce than in the wholesale market suggesting some stability if taken in isolation. However, it is likely that retail prices will fall in line with the wholesale market heading into Q3 2019 as demand for hybrid, plug-in hybrid and BEVs continues to increase as increasing volumes change hands.

BEV a trickle to full bore in 2020

With total cost of ownership arguably more advantageous for BEV than their ICE counterparts and many cities in the UK already incentivising their use such as London and Milton Keynes, BEVs are becoming ever more attractive to new and used car buyers in the UK. Dealers continue training courses offered by manufacturers and industry bodies such as the National Franchise Dealer association whilst independent dealers are ensuring they remain in the mix as they update their knowledge about this burgeoning segment of the market.

Leasing companies are also considering remarketing the vehicles 2 to 3 times through additional leases whilst reconditioning the battery when required.

Range anxiety continues to diminish as more and more drivers start to understand the physics involved with driving any car, whether it has an internal combustion engine (ICE) or a BEV, range varies with use whilst hot and cold weather driving also requires energy to heat or cool the vehicle. One of the greatest advantages of BEVs is that you can generate energy whilst on the move. Just like an ICE car, a BEV will use energy going up a hill, but on the way down it can convert kinetic energy into electrical energy adding a little to the vehicle’s range.

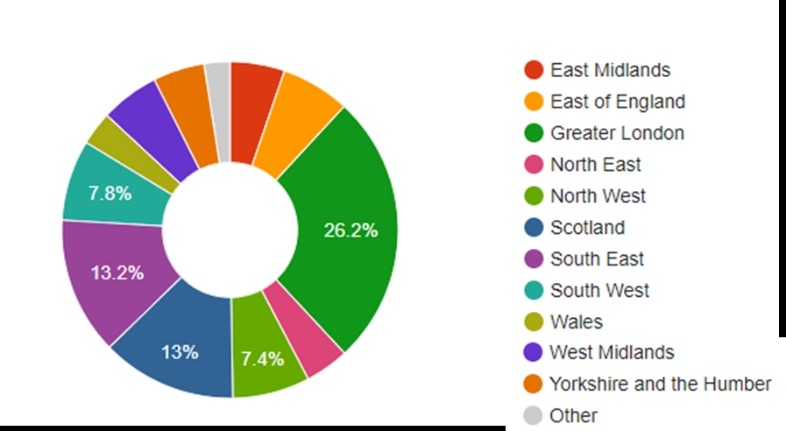

In the UK, infrastructure continues to be a point of discussion. As of the 24 July 2019, according to Zap-Map.com, there are 2,321 public rapid charging devices in 1,593 locations across the UK with 24,682 public chargers in total.

The pie chart above shows the breakdown of public charging point connectors in each of the UK regions. London and the Southeast have the most charging points followed by Scotland; the regions with the least charging points are Yorkshire and Wales.

Source https://www.zap-map.com

The charging infrastructure needs to improve, especially destination chargers when the car would be stationary for extended periods, for example in work carparks, whist drivers are shopping or at the cinema. However, we need to remember that drivers can charge a car at any of 40 billion 3-pin plug sockets across the UK and home charging is where 95% of BEV charges currently take place.

Heading into 2020, the main stimulus for BEV demand in the UK will from fleet and business drivers with the reduction of benefit in kind (BIK) taxation rates for company car drivers. Announcing this month, the UK government confirmed that company car drivers choosing to drive a BEV would pay no benefit-in-kind tax in 2020/21. This will have met with universal approval whilst giving manufacturers confidence to ramp-up production for the UK market.

With BIK rates for BEVs only increasing by 1% per year for the following two years, the Glass’s team forecast significant increases in demand for BEVs.

Range anxiety may always be an issue for some drivers whilst conventional fuel types still hold the market, but with the BEV market share rising, the future is beginning to look electric.