Close

Close

Battery-electric vehicles (BEVs) experienced a difficult January across many of Europe’s major used-car markets. Autovista Group experts consider powertrain performances, including residual value (RV) trends and days to sell.

RVs of all-electric models presented as a percentage of the original list price (%RV), experienced a troubled start to 2024. Set against a market average covering all powertrains, BEVs retained considerably less value across a number of European countries.

The biggest gap was recorded in Italy, where all-electric models only retained 37.8% of their new-car value after three years and 60,000km. Meanwhile, the average across all powertrains in the country sat at 55%.

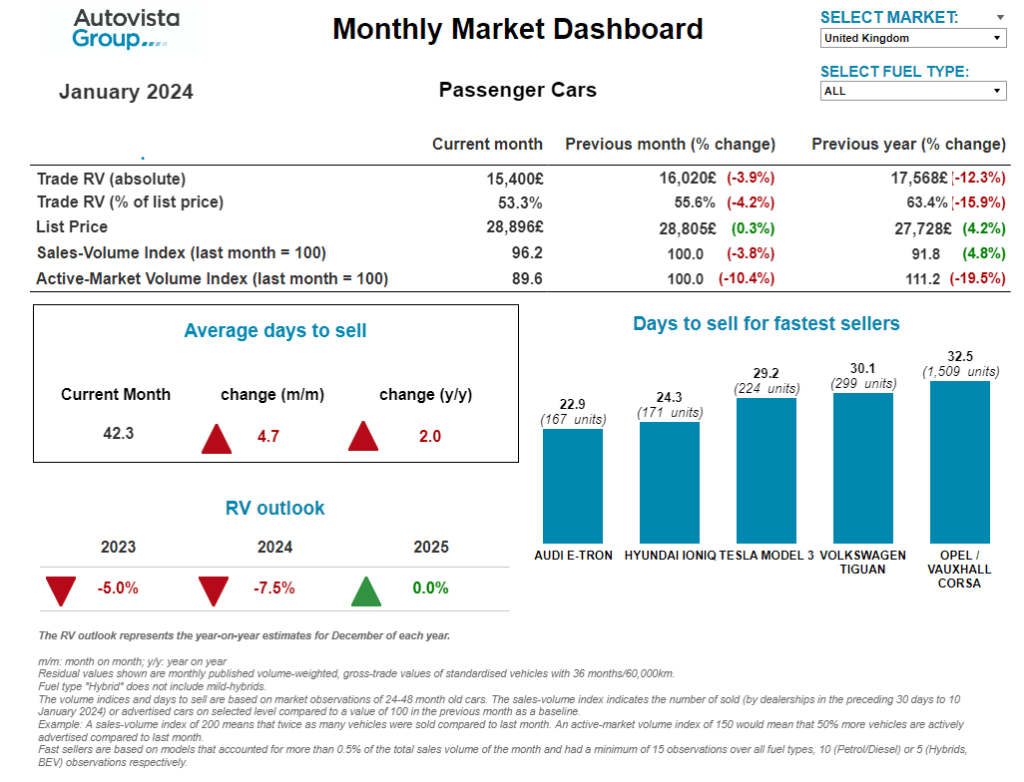

BEVs saw a similar performance in the UK, with value retention levels at 38.4%, while the total market average sat at 53.3%. Used all-electric cars retained 41.7% of their value in Germany while all powertrains averaged 51.6%.

The electric powertrain saw %RVs hit 47.3% in Austria, compared with 53% across the wider market. In Switzerland, BEVs retained 44.9% of their new-car list price. This resulted in a more favourable comparison against the wider market, which recorded an average %RV of 49%.

Of the markets up for review, Spain was the only one to see BEVs retain over half of their original list price in January. But at 50.2%, this did equate to a larger gap in relation to the market average of 60.2%.

The interactive monthly market dashboard examines passenger-car data by fuel type, for Austria, Germany, Italy, Spain, Switzerland, and the UK. It includes a breakdown of key performance indicators, including RVs, new-car list prices, selling days, sales volume and active-market volume indices.

Do EVs need a boost?

These latest figures coincide with troubling headlines about electric vehicle (EV) uptake, as demand appears to have dipped across new-car markets. Companies originally keen to electrify their fleets have contributed to this more negative narrative.

Within its fourth quarter results, Hertz confirmed its plan to reduce the presence of EVs in its fleet. ‘We continued to face headwinds related to our electric vehicle fleet and other costs throughout the quarter,’ said Stephen Scherr, Hertz chair and CEO.

‘We have taken steps to address those challenges and heading into 2024, we are confident that our planned reduction in EVs and cost base, along with the ongoing execution of our enhanced profitability plan, will enable us to regain our operational cadence and improve our financial performance with increasing effect into 2025,’ Scherr added.

However, there are some signs of redemption for all-electric cars, as BEVs topped the fastest sellers list in two major used-car markets. The Audi e-Tron was sold in an average of only 23 days in the UK, while in Germany the Volkswagen ID.3 needed 42 days.

With year-on-year growth posted in the sales-volume index (SVI) across all six markets, demand for the powertrain does remain. So, while BEV prospects might appear bleak at first, consumers in the used-car market do seem willing to snap up the right model at an attractive price.

A turning point for UK BEVs?

‘Following poor trading conditions throughout December 2023, a three-year-old car’s average %RV fell,’ confirmed Jayson Whittington, Glass’s (part of Autovista Group) chief editor, cars and leisure vehicles.

At the beginning of January 2024, %RVs dropped to 53.3% from 55.6% in December 2023. Compared to 12 months earlier, levels declined by over 10 percentage points, a stark reminder of just how volatile the used-car market has been over the past year.

All powertrains experienced significant declines in %RVs over the past 12 months, although some stood out more than others. ICE-powered models fared better than electrified vehicles, with petrol falling 8.8 percentage points year on year. Meanwhile, diesel declined slightly less at 8.3 percentage points.

In recent years, HEVs retained significantly more of their cost-new price than other powertrains, however, this has since been eroded. HEV %RVs fell by 15.8 percentage points compared to last year and is only marginally ahead of petrol at 55%. PHEV %RVs fell 12.6 percentage points, down to 50.9%.

BEVs recorded the most noteworthy %RV performance in the past 12 months. Figures fell by 20.7 percentage points, from 59.1% to just 38.4%. All-electric RVs have now settled, and their revised price position is proving popular with consumers. This has been illustrated by the list of fastest-selling models which has included BEVs in the past few months.

According to the SVI, sales activity for the overall market was down 3.8% in the 30 days prior to 10 January 2024, compared to December. This is perhaps unsurprising as consumers tend to have other priorities during this period. However, the SVI was up 4.8% from a year earlier.

Dealers will be hoping that the used-car market will begin to improve and that RVs will stabilise. Early indications are that the wholesale market improved in January. So, dealers clearly have the confidence to stock forecourts, which bodes well.

Slight RV rise in Austria

Lower levels of used-car transactions persisted in Austria as living costs remained high. In January, the SVI fell by 16.5% compared with December, and 6.5% year on year. At the same time, the supply volume of two-to-four-year-old passenger cars was around 2.7% lower than in December 2023.

The average number of days needed to sell a used car increased to nearly 71 days in January. Diesel vehicles sold the fastest, averaging approximately 62 days, followed by petrol cars at 74 days. Plug-in hybrids (PHEVs) sold at around 84 days, and battery-electric vehicles (BEVs) at just over 89 days. Full hybrids (HEVs) posted slower sales at nearly 96 days.

Despite weakening demand, the %RVs of 36-month-old cars increased slightly compared to December, reaching 53% on average. This marked a decrease from 54.9% in January 2023 and shows that pressure on RVs is increasing alongside stable used-car supply.

HEVs led the way with a %RV trade value of 57.2% followed by petrol models (55.5%), diesel cars (51.9%) and PHEVs (50.7%). Meanwhile, 36-month-old BEVs retained the lowest value, at 47.3%. As demand is expected to weaken, further pressure on RVs can be expected.

‘The market’s average %RV of a 36-month-old car at 60,000km ended last year down 4.6% on December 2022,’ Robert Madas, Eurotax (part of Autovista Group) regional head of valuations, Austria, Switzerland, and Poland outlined.

‘In 2024, %RVs are expected to decrease further by around 3.4% year on year, due to weakening demand and unwavering supply. In 2025, %RVs are expected to decrease but at a slower pace,’ he reflected.

Savage EV spiral in Germany

Absolute RVs in Germany remained stable month on month but dropped 7.7% compared with January 2022. With list prices increasing, %RVs declined 4.6% against December and 10.6% year on year.

The country’s new-BEV market has struggled recently. This follows the abrupt halt of purchase incentives in mid-December. In January, the used-car market saw all-electric %RVs fall to 41.7% from 51.9% a year earlier.

‘At the end of 2023 and into January 2024, news of large manufacturer discounts and price reductions for electric vehicles (EVs) dominated discourse across the automotive industry,’ highlighted Andreas Geilenbruegge, head of valuations and insights at Schwacke (part of Autovista Group).

This sends out a dire message to potential electric customers: ‘something is wrong with EVs and nobody wants them.’ The concern is that this perception becomes reality as popular opinion turns against the technology, slowing uptake and generating further scepticism.

In turn, dealers have become unsettled as stock volumes increase and days to sell extend. Of the younger used cars on the market from 2022 onwards, roughly one in six is a BEV or PHEV. This trend, alongside the associated risks, is increasing.

‘Prices are falling and competitive pressure is ensuring continued downward momentum. Decreasing new-car prices have only served to accelerate this trend. This will negatively affect models registered between 2020 and 2023 as they enter the used-car market,’ Geilenbruegge added.

The only way to ensure some RV stability in the country is by reducing or delaying volumes via exporting or used-car leasing. Dealers will need support from manufacturers to ensure adequate prices can be maintained until buyers are found.

Ultimately, this negative trend can only be tempered by external stimulation generating more used-car demand. However, five out of six young used cars are still quite profitable. This is thanks to their internal-combustion engine (ICE) powertrain, not to mention those registered before 2020.

Italy awaits EV incentive announcement

Overall, Italy’s used-car market performed as expected in January. Absolute RVs grew by 9.1% year on year, but list prices increased by 9.9%. Therefore, %RVs saw a slight fall of 0.7%.

This descent is only expected to become more severe, reaching a drop of 2.2% by the end of 2024. Given the normalisation of factors which led to strong RV growth in recent years, this downward trend is forecast to continue.

‘However, one factor could change this scenario considerably, namely a new incentive scheme that could be introduced in the coming weeks, potentially in March,’ explained Marco Pasquetti, head of valuations, Autovista Group Italy.

The decree has still to be discussed, but some potential details have come to light in statements made by the Ministry of Enterprise and Made in Italy. Citizens with an annual income below €30,000 could scrap an older vehicle (up to Euro 2) and receive €13,750 towards a new EV purchase. This is more than double the current incentive.

This would likely put far more pressure on RVs, which would fall faster than expected. There has also been some talk of incentives for used cars. However, it is necessary to wait for a final official text before drawing up any conclusions.

EVs still sluggish in Spain

‘It is common for the first month of the year to see a downward adjustment in used-car prices, but at the start of 2024, this added to a negative trend already set in motion in 2023,’ commented Ana Azofra, Autovista Group head of valuations and insights, Spain.

The average absolute RV of a used vehicle fell by 0.9% from December 2023 to January 2024. This was particularly driven by the declining values of PHEVs and BEVS, down 2.1% and 1.4% respectively. EVs have not yet taken off in Spain, despite government incentives.

‘Price adjustments of new models will help remove the economic barrier, but the lack of appropriate charging infrastructure remains a significant obstacle to market integration,’ Azofra confirmed.

Combined sales of new BEVs and PHEVs just about reached a 12% market share across 2023. This is increasingly distant from the European EV average, only similar to Italy, where growth has slowed in recent months.

Yet the number of BEVs on offer continues to expand alongside the pressure to sell them. Leasing companies are integrating these models into their fleets, but rental companies are starting to go the opposite way, despite their importance in southern European markets.

This is increasing the volume of used EVs entering dealerships, where they are still difficult to sell. Therefore, the pressure on used plug-in models is intensifying, with this downward trend expected to continue in the coming months.

Other powertrains have seen more balanced trends in recent months, with HEVs dominating the market and possibly already approaching a natural ceiling. Toyota’s Yaris and C-HR once again saw the best turnover data in January.

EVs struggle in Switzerland

With higher living costs in Switzerland since the beginning of 2023, used-car transactions have struggled over the last 12 months. The country saw its active-market volume index for two-to-four-year-old passenger cars fall by 2.5% month on month. This more than doubled year on year to a decline of 5.5%.

Remaining in stock for 79 days, two-to-four-year-old passenger cars sold slightly faster last month, down a day from December. HEVs were once again the fastest selling on average, after around 58 days, followed by diesel cars (70 days), then petrol models (78 days). EVs took longer to move, as BEVs took over 92 days to sell and PHEVs needed nearly 94 days.

HEVs achieved another slight year-on-year %RV gain, holding firm at 52.6%. Petrol cars came next (49.9%), then diesel models (48%), followed by PHEVs with 46.3%. 36-month-old BEVs held 44.9% of their original list price.

The SVI in Switzerland declined significantly in January, down 16.9% month on month and 13% year on year. Meanwhile, the average %RV of a 36-month-old car declined again, as supply remained stable and demand deteriorated. Figures dropped from 49.4% in December to 49% in January, moving further away from the 52.6% recorded a year earlier.

Three-year-old car values are forecast to decline from a relatively high level, set against a wider declining trend,’ commented Hans-Peter Annen, head of valuations and insights, at Eurotax Switzerland. ‘Used-car demand is expected to weaken while supply remains steady.’

This content is brought to you by Autovista24.