Close

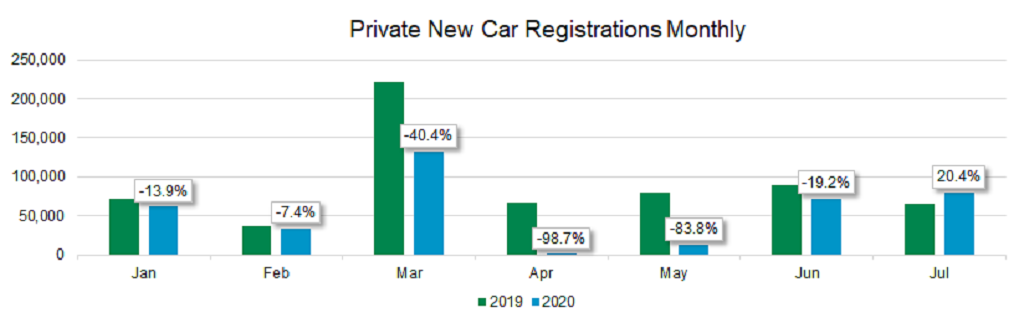

CloseAccording to registration figures released by the SMMT, the UK’s new car market recorded its seventh monthly decline in August with a 5.8% reduction compared to last year. Fortunately, as August tends to be a low volume month, the reduction equates to only 5,347 units. Year to date, total registrations now sit 39.7% lower than 2019 at 915,615 cars.

There is little prospect of clawing back lost ground due to lockdown. However, September’s plate change could offer some good news if the new ’70-plate’ produces a bumper registration haul and exceeds last year’s total. There are suggestions from the industry that if new car stock allowed, September could record the highest number of registrations ever, due to resurgent demand. This positive market sentiment is incredible for a market so severely affected during the lockdown, however, in reality, COVID-19 related production and logistical related delays will likely rule out a record September.

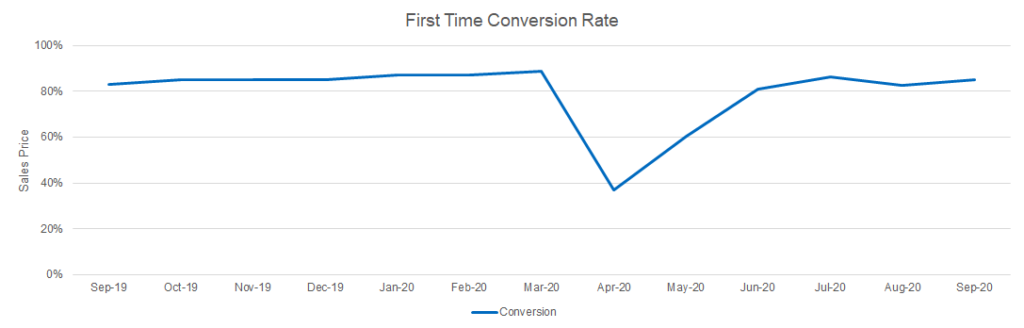

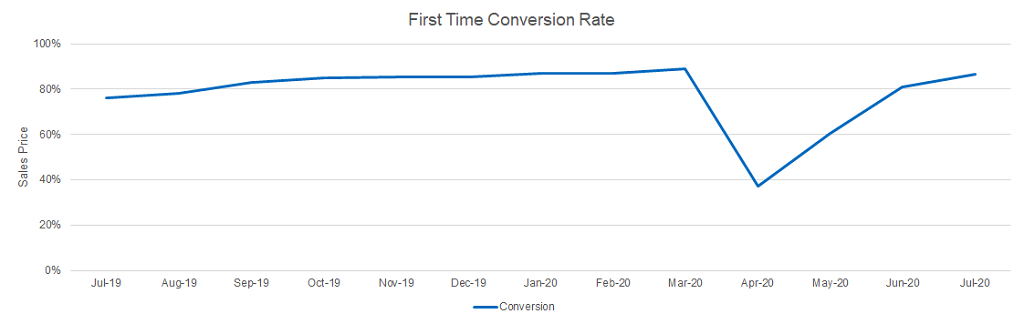

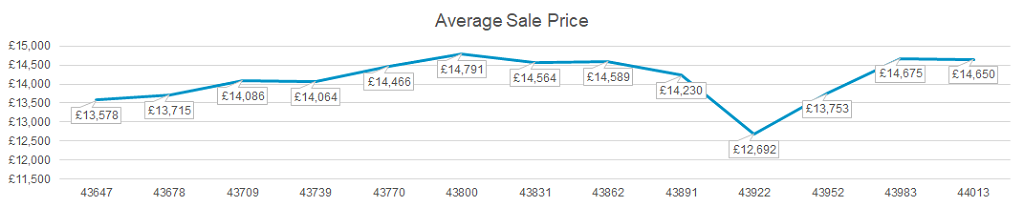

The used car market continues to outperform last year with auction activity in August remaining strong. The average first-time conversion rate was 82.8% which is almost five percentage points better than in August 2019. Hammer prices remained high in August, exceeding Glass’s Trade values by 2.3%, leading to further increases in Guide values in September. This compares to a reduction in September last year of 2%, underlying how different this year is compared to last.

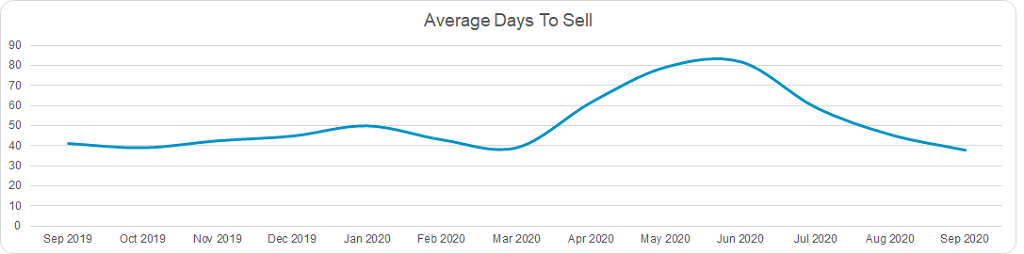

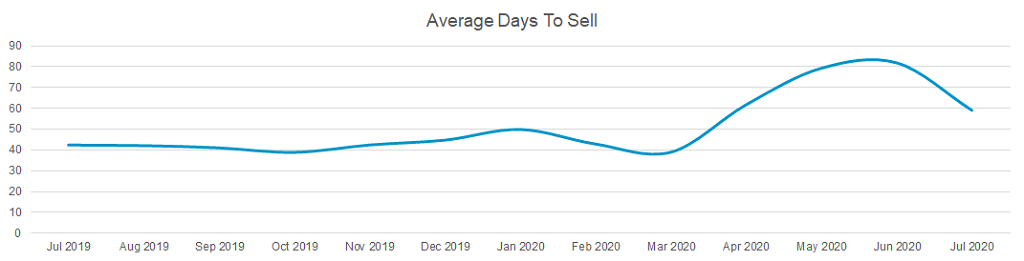

The buoyant retail market continues to underpin strong trade market conditions. Following the trend since the end of lockdown, average days to sell retail units continued to reduce in August. The average fell to 45 days down from 59 days in July and is now tracking pre-lockdown levels.

Whilst increased new car sales activity through September is expected to generate more part exchanges, it is unlikely that they will hit auction sales in volume until the back end of the month. We, therefore, expect wholesale trading conditions to remain strong throughout September.