Close

CloseDespite increases in some European markets during April, demand for used cars plummeted in May, impacting residual values (RVs). Autovista24 journalist Tom Hooker reviews the data with Autovista Group experts.

Used-car demand dropped significantly across major European markets last month. The sales-volume index (SVI) of two-to-four-year-old cars fell in Germany, Spain, France, Switzerland, Italy and Austria compared to April. Alongside the UK, most of these countries also suffered a year-on-year sales decline.

Germany saw the sharpest drop compared to April, with demand slumping by 35.5%. Spain endured a 32.5% decline, while the SVI in France fell by 21.2%. Sales in Switzerland declined by 13.4%, followed by Italy and Austria, where demand dropped by 12.8% and 11.6%, respectively.

The UK was an outlier, avoiding a month-on-month decline, although its SVI increased by just 0.2%. However, when compared to May 2024, demand in the UK decreased by 23.7%.

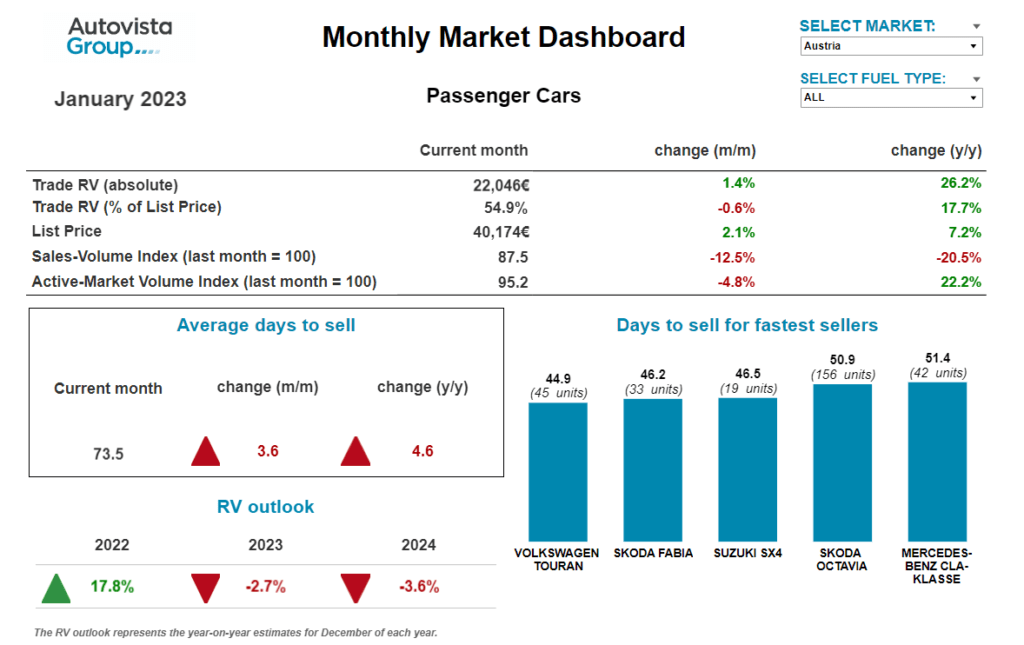

Click here to view the full Monthly Market Dashboard

This was far from the greatest year-on-year decline, with dealership sales in Spain slumping by 66.4%. In Germany, two-to-four-year-old models endured a 33.2% drop in demand, according to the SVI. Meanwhile, Austria and Switzerland both saw this metric fall by 13.7%. How did this apparent decline in demand affect other metrics?

Residual values fall further

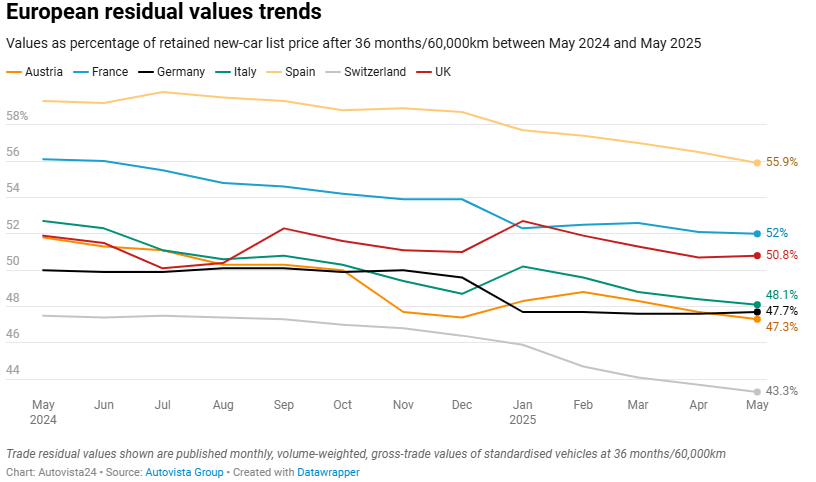

RVs presented as a percentage of original list price (%RV) after 36 months and 60,000km, continued their decline in May. As the market is experiencing relatively stable supply, declining consumer demand is placing additional pressure on RVs. These values are forecasted to drop across Europe this year.

Most of the markets under observation have seen %RVs fall since the start of the year. The only exception is Germany, which has recorded value stability since January.

Italy saw the biggest year-on-year decline in %RVs, with values dropping by 4.6 percentage points (pp) compared to May 2024. Austria was next, down 4.3pp, then Switzerland, dropping 4.2pp.

Spain saw values dip by 3.4pp, while Germany recorded a decline of 2.3pp. Of the recorded markets, the UK saw the smallest year-on-year change in %RVs, down 1.1pp.

Rising list prices

May witnessed a rise in list prices. All markets recorded an increase in this metric compared to April.

The UK had the biggest increase of 3.1%, followed by France up 2.3%. List prices in Spain grew by 1%, while Germany, Austria and Switzerland all posted a 0.7% rise in this metric from one month ago.

Italy had the smallest increase compared to April, up just 0.2%. It recorded a drop in list prices compared with May 2024, down by 2.3%. In contrast, list prices grew by 9.3% in Austria compared to one year prior.

The UK also saw a steep increase of 7.8%, while cost-new prices in Spain and Germany rose by 7.5% and 7.2% respectively. Meanwhile, list prices grew by 5.1% in Switzerland.

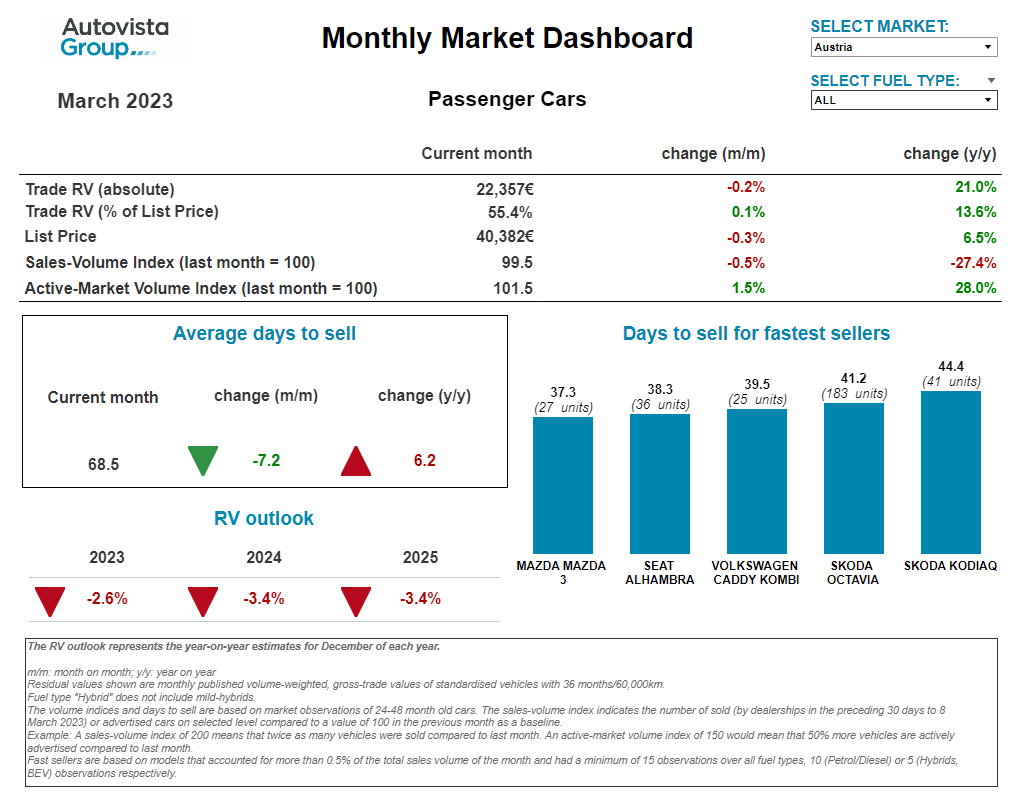

Demand drops in Austria

‘The SVI in Austria decreased in May following an increase in April. The number of observed sales fell by 11.6% compared to the previous month. This equated to a year-on-year decline of 13.7%,’ stated Robert Madas, Autovista Group’s regional head of valuations.

Meanwhile, the active-market volume index (AMVI) of two-to-four-year-old passenger cars decreased slightly, down 3.1% compared with April. The number of adverts for passenger cars in this age bracket fell by 6% compared to the previous year.

At 65 days, the average amount of time needed to sell a used car remained consistent in May.

Diesel vehicles continued to be the fastest-selling powertrain, taking 58.9 days on average to sell last month. This was followed by plug-in hybrids (PHEVs) at 65.9 days, petrol vehicles at 67.2 days and full hybrids (HEV) at 67.8 days. Battery-electric vehicles (BEVs) took the longest amount of time to sell at 81.1 days.

Average %RVs decreased marginally to 47.3% in May. This was a 0.3pp drop compared to April but a slump of 4.3pp year-on-year.

‘HEVs retained the greatest amount of trade value in January at 51%, followed by petrol cars at 49.2%. Then came diesel models with 47.7% and PHEVs with 45.6%. BEVs again retained the lowest amount of value, at 39.9%. This was its second consecutive monthly drop, so the improving trend for BEVs has ended,’ highlighted Madas.

%RVs are expected to decrease in the coming years but at a slower pace. This is due to weakening demand and unwavering supply. By the end of 2025, %RVs are expected to decrease by 0.6%. In 2026, a slight year-on-year drop of 0.7% is also expected.

Expensive used cars in France

%RVs were roughly stable in May, with a very slight decrease. The 2% absolute RV growth was mainly because more expensive cars were sold this month. List prices increased by 2.3% compared to April.

Petrol-powered vehicles remained stable, as the fastest sellers came from A, B and B SUV segments. The diesel market also stayed relatively unchanged, with the fastest movers coming from the C SUV and D segment.

‘Overall, HEV %RVs decreased slightly in May, as increasingly expensive vehicles were sold. Newer and more expensive models in this category do not hold values as well as older hybrid cars, which were on the market when the technology was still emerging,’ commented Ludovic Percier, Autovista Group’s senior RV analyst for France.

PHEVs also suffered a slight %RV drop. Used-car customers are not willing to pay such a high premium, like for HEVs. Supply for the technology still exceeds demand, causing %RVs to fall in the last few months.

The only thing holding %RVs is the release of new models with better electric-only ranges alongside more premium vehicles. Yet, list prices on the new-car market remain high, explaining the powertrain’s larger value loss.

Stagnating BEVs

BEV %RVs suffered a marginal decline in France as more expensive vehicles were sold in May. In this category, the Tesla Model Y was the quickest to sell. However, the sedan’s price, along with its Model 3 sibling, dropped recently.

Most of the fastest-selling BEVs were more affordable models or those offering the best ratio of price and range. This was highlighted in the fastest-sellers list with the Smart Fortwo and BMW i3 taking second and fourth respectively. Elsewhere, premium BEV cars struggled to hold value like their ICE equivalents.

‘The technology appears to be stagnating, as brands are pushed by governments to sell an increasing number of new BEVs. This means the used-car market is becoming crowded with these models but still has too few buyers,’ noted Percier.

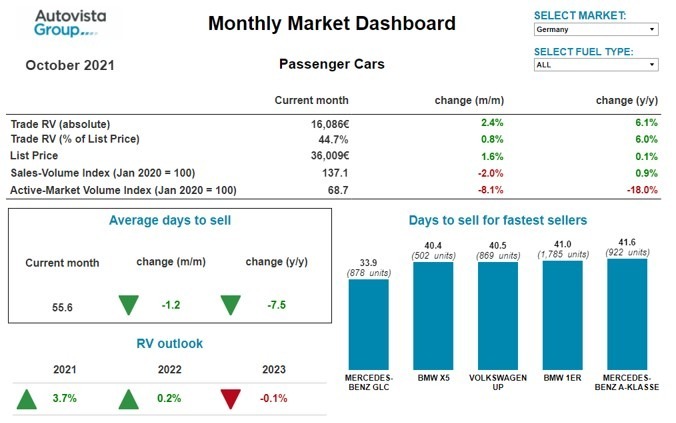

Germany’s declining demand

Following a significant increase in April, the SVI suffered a steep decrease in May. Compared to the previous month, this metric was down 35.5%. It also endured a 33.2% drop year-on-year.

Meanwhile, the AMVI of two-to-four-year-old passenger cars remained rather stable compared to April with a slight decrease of 1.3%. The supply volume of passenger cars in this age bracket dropped by 11.5% compared to the previous year.

‘The average number of days needed to sell a used car decreased to 58 days in May. PHEVs sold the fastest at 54.5 days, while diesel cars also sold quickly, taking 55.6 days on average. Then came HEVs at 56.4 days, followed by BEVs after 57.7 days and petrol cars after 60.4 days,’ said Madas.

%RVs of 36-month-old cars at 60,000km showed a marginal increase in May. Used models held an average %RV of 47.7%, up 0.1pp from April. Petrol cars led the market with a %RV of 49.3%. Then came HEVs at 48.8% and diesel cars at 48.7%, followed by PHEVs at 42.7%. BEVs again retained the lowest level of value at 37.2%.

‘Although RVs have stabilised recently, demand remains rather weak. Therefore, RVs can be expected to remain under pressure. In 2025, %RVs are forecast to decrease, down 2.8% when compared with December 2024. Pressure will probably ease in 2026, with RVs forecasted to decline by 1.4%,’ he outlined.

Positive growth in Spain

Spanish new-car sales continue to perform positively, with a growth of 7.1% in April. This meant the market surged 12.2% during the first four months of the year.

All channels saw registration growth. The corporate channel improved at a steady pace and the rental channel grew at a higher rate. This boost in sales came ahead of the start of the peak tourist season.

‘The private individual channel also increased in volume. This was largely due to the special Reinicia Auto+ plan for those affected by the DANA floods in Valencia. A boost in EV deliveries also helped. The technology reached a 16.2% share in May while representing 14.7% of total sales in the year to date,’ explained Ana Azofra, Autovista Group’s head of valuations and insights, Spain.

The used-car market is also experiencing a period of growth, up 3.7% from January to April. Furthermore, there was a significant increase in EVs and younger cars being sold in this period. This creates a more sustainable used car offer.

‘Regarding average transaction prices, the Spanish market continues to distance itself from the negative trend observed in most European markets. All powertrains saw values stabilise, while used cars sold 10 days faster on average when compared to the previous year, taking 67.3 days. So, we can continue to expect stability,’ noted Azofra.

Only PHEVs and petrol models showed a drop in absolute RVs during May, falling by -4.7% and 0.4% respectively. However, it is worth noting that the mix of PHEV cars in Spain now includes offerings from more economical segments and brands. The fastest-selling models in May were the Lynk & Co 01, Kia Ceed and Toyota CH-R.

Switzerland’s significantly lower demand

‘After an increase in April, the SVI decreased significantly in Switzerland during May. The number of sales observed decreased by 13.4% compared to the previous month. Year-on-year, the SVI was down by 13.7%,’ stated Madas.

Meanwhile, the AMVI of two-to-four-year-old passenger cars decreased by 1.1% compared to April. However, the supply volume of passenger cars in this age bracket slumped by 11.7% compared to the previous year.

RVs of 36-month-old cars at 60,000km dropped slightly in May, as %RVs fell to 43.3% from 43.7% in April. Yet, the year-on-year drop was more severe, down 4.2pp from the values recorded 12 months ago.

‘HEVs retained the most value in May by far at 48.4%. Then came petrol cars at 44.7%, diesel models at 42.1% and PHEVs at 40.7%. BEVs were once again the worst-performing powertrain, retaining just 37.3% of their original list price after three years and 60,000km,’ he highlighted.

April saw two-to-four-year-old passenger cars sell at a similar pace to April. On average, used vehicles spent 73.9 days in stock.

HEVs sold fastest at 57.2 days, followed by petrol cars at 72.3 days, diesel models at 75 days and BEVs at 79 days. Meanwhile, PHEVs needed the most time to sell at 84 days on average.

A trend of relatively stable supply and low demand will continue as various uncertainties shroud 2025. Therefore, %RVs are expected to decrease in the next years, but at a slower pace. By the end of 2025, %RVs are predicted to decrease by 3.9% compared to December 2024. In 2026, a lower year-on-year drop of 1.5% is forecast.

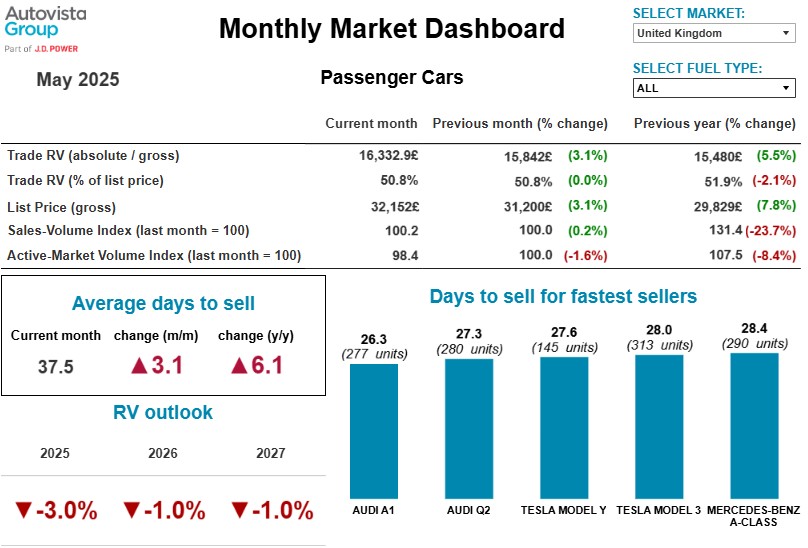

Stability in the UK

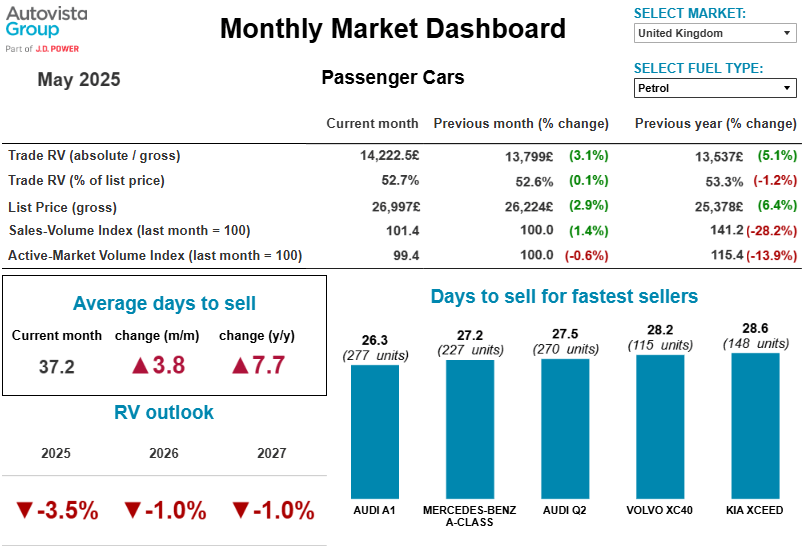

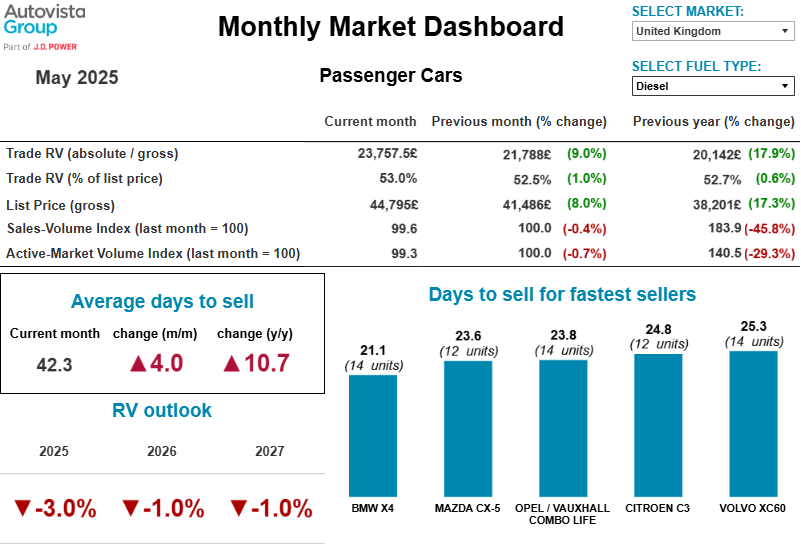

In May 2025, the average three-year-old car retained 50.8% of its original cost-new price. This was unchanged from April, indicating a stable used car market. The average %RV of petrol cars increased marginally by 0.1pp to 52.7%, while the average %RV of diesel cars rose by 0.5pp to 53%.

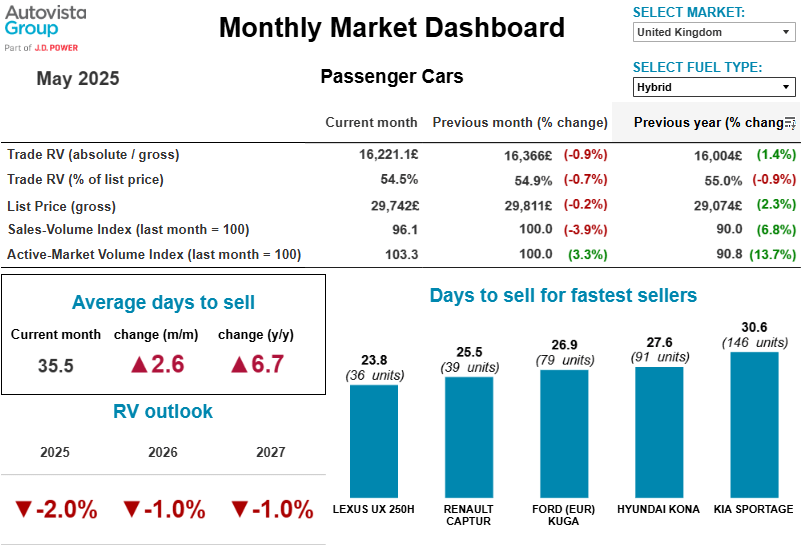

‘In contrast, the average hybrid model retained 54.5% of its original list prices, a drop of 0.4pp, and the average PHEV %RV decreased by 0.6pp to 49.2%. BEVs saw a slightly larger drop, with the average RV falling by 0.9pp to 37.5%,’ said Jayson Whittington, Autovista Group’s regional head of valuations, UK.

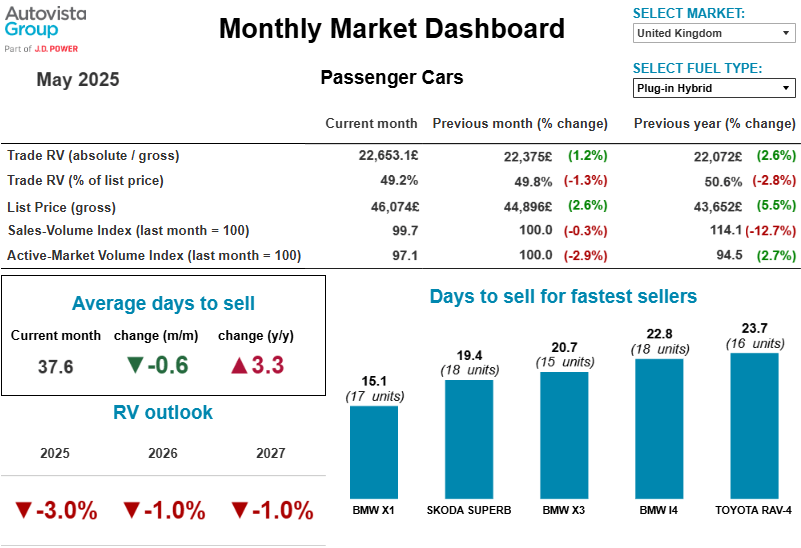

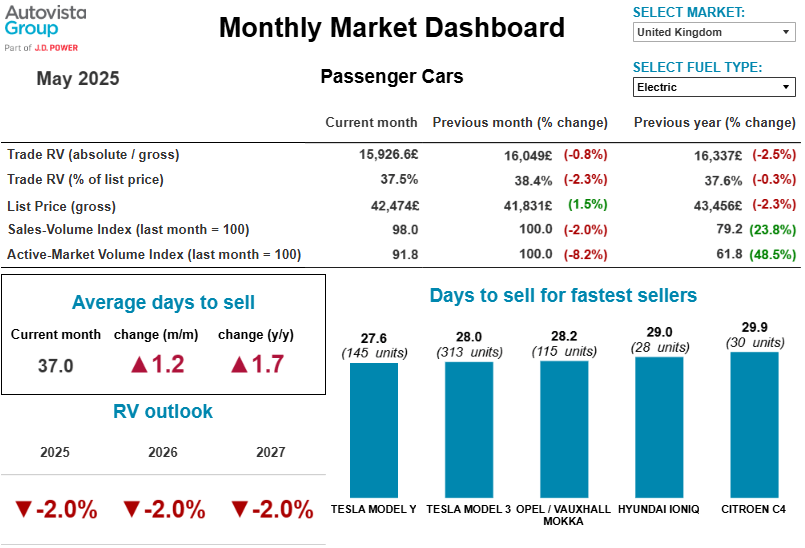

On average, it took 37.5 days to sell a used car in May, an increase of 3.1 days month on month. Hybrid cars emerged as the fastest-selling fuel type in the UK, with an average sales time of 35.5 days. They also retained the largest percentage of their original list price after three years.

Hybrids slower to sell

The average number of days needed to sell a used petrol car rose by 3.8 days to 37.2 days. For diesel, this metric increased by 4 days to 42.3 days.

Although hybrid vehicles performed well overall, it took 2.6 additional days to sell one in May compared to April. PHEVs took 0.6 fewer days to sell at 37.6 days. It took dealers on average 37 days to sell a BEV, up 1.2 days month on month.

The SVI remained broadly level compared to April, indicating consistent retail conditions. Meanwhile, the AMVI showed a 1.6% decrease in the number of cars advertised for sale by dealers.

‘If March’s plate change activity generated additional used cars, they have either already washed through forecourts, or the volume was not substantial, and with no significant extra volume expected to hit wholesale channels, the short-term outlook for RVs in the UK is stable,’ concluded Whittington.

The content is presented to you by Autovista24