Close

CloseFollowing a strong month of new-car registrations in March, the UK government is looking to further support the country’s automotive market. But will changes to the ZEV mandate reduce pressure on carmakers? Autovista24 special content editor Phil Curry examines the data.

After five consecutive months of decline, the UK’s new-car market bounced back in March. With the country’s ‘new-plate’ month often producing larger registration volumes, this year saw electrified vehicles benefit.

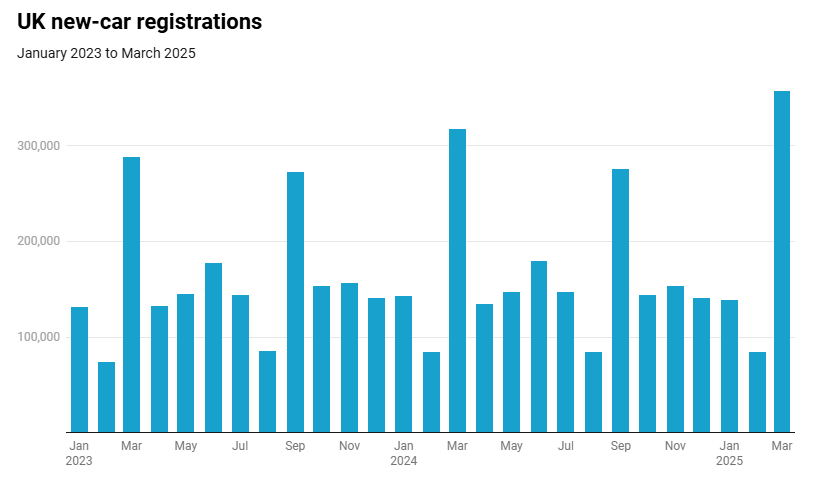

The latest data from the SMMT reveals that UK new-car registrations grew 12.4% in March. A total of 357,103 units were delivered to customers, up by 39,317 deliveries year on year. This is the best March total since 2019 and brings an end to a run of declines stretching back to October 2024.

The performance caused a turnaround in the market’s year-to-date fortunes. Over the first three months of 2025, the market returned to growth, with registrations up 6.4%. A total of 580,502 new cars were delivered over the first quarter, up by 34,954 units year on year.

However, the market is far from stable at present, and the stricter zero-emission vehicle (ZEV) mandate target for this year has caused concern in the industry.

Together with the upcoming 2030 petrol and diesel new-car ban, pressure on the market has increased in recent months. Yet, new announcements by the UK Government are aimed to alleviate these concerns.

The path to 2030

In the wake of global political and financial turmoil, the UK government has announced measures to boost the new-car market. Alongside a relaxation in the rules around the 2030 petrol and diesel new-car ban, it is also revising the ZEV mandate. Targets remain, but the opportunities to avoid financial penalties are increased.

Pure internal-combustion engine (ICE) models will be banned from new car sales in 2030. However, both full hybrid (HEV) and plug-in hybrid (PHEV) models will continue to be sold until 2035. Carmakers will need to ensure that overall CO2 emissions from these models are 10% lower than their 2021 levels.

Meanwhile, in the light-commercial vehicle market, petrol, diesel, HEV and PHEV sales will continue until 2035. Manufacturers must ensure that CO2 emissions between 2030 and 2035 do not grow above levels from 2021.

Small-volume manufacturers with registrations between 1,000 and 2,499 units and micro-volume manufacturers with registrations under 1,000 units will be exempt from the 2030 to 2035 hybrid requirements. These businesses will need to meet a nominal CO2 reduction across their fleets during this period, which will be agreed upon individually.

Flexibility in the ZEV mandate

When it comes to ZEV mandate targets, to reduce the pressure on carmakers in the UK, the government has reduced the fine-per-unit over the required target. Manufacturers will now pay £12,000 (14,006) per car over the zero-emission model threshold, a drop of £3,000.

The flexibilities to transfer credits between car and van markets and from less-polluting models have also changed.

In the new plans, one car credit can be exchanged for 0.4 van credits, while one van credit can be exchanged for two car credits. This is derived from relative mileage and CO2 emissions. This flexibility would be uncapped and available from 2025 onward.

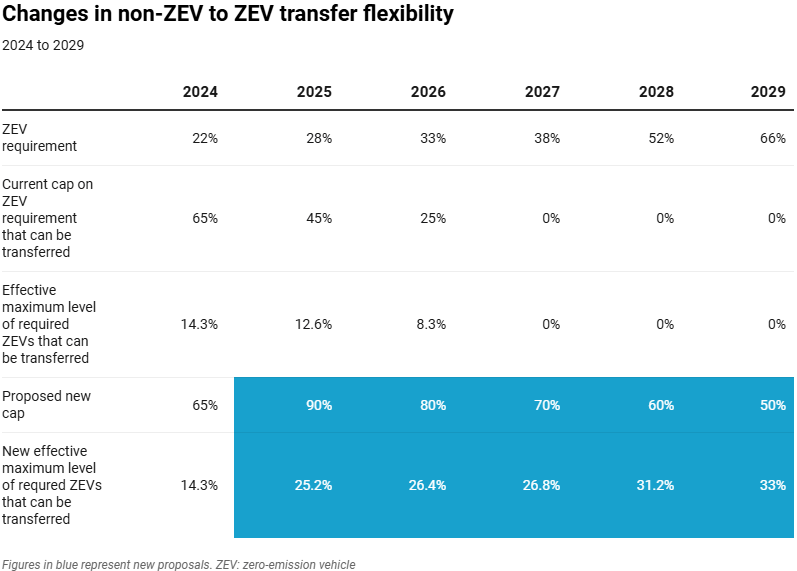

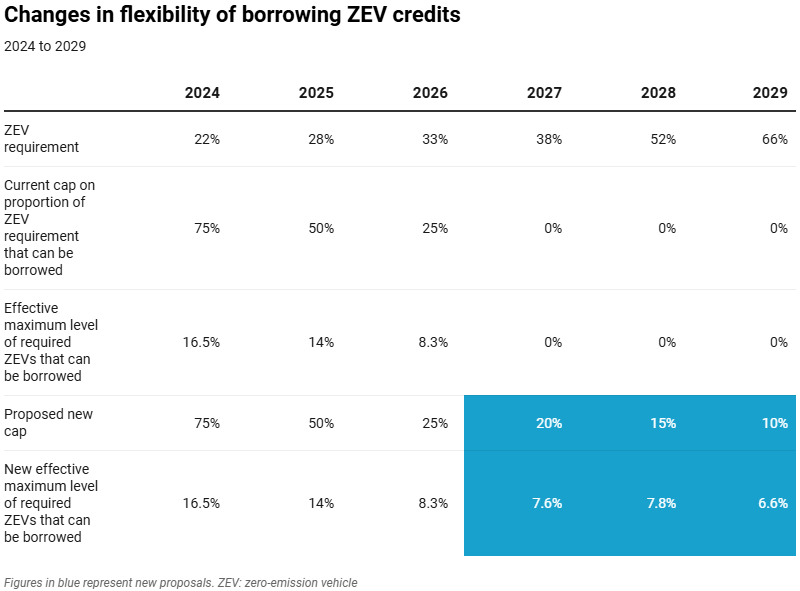

Currently, carmakers can create credits by cleaning up their non-ZEV fleet compared to their 2021 CO2 baseline. This ability was set to expire next year, but will now be extended to 2029. Therefore, manufacturers now have the flexibility to reward any CO2 savings from their hybrid fleets towards their ZEV targets.

However, this flexibility will be capped each year, ensuring the mandate continues its goal of driving zero-emission sales.

In 2025, the original emissions flexibility was capped at 45% of the total ZEV requirement. This has now doubled to 90%. Therefore, 25.2% of a carmaker’s fleet target can be made up of non-ZEV cars based on emissions trading credits.

The cap drops by 10 percentage points each year until 2029, when it reaches 50%. The existing ZEV mandate targets remain, yet the push for more HEV and PHEV options in carmaker line-ups should allow for enough emissions trading to reduce the likelihood of penalties.

The period where credit borrowing from other manufacturers is also extended to 2029, with the borrowing threshold dropping each year. From a 50% maximum in 2025, the cap falls to 25% in 2026, and then by 5pp each year until it reaches 10% in 2029.

The industry reacts

‘The government has rightly listened to industry, responded quickly to global dynamics and recognised the intense pressure manufacturers are under,’ commented SMMT chief executive Mike Hawes.

‘Industry remains committed to decarbonising road transport, but the ZEV mandate targets are incredibly challenging, especially with a paucity of consumer demand and geopolitical upheaval.

‘However, growing electric vehicle (EV) demand to the levels needed still requires equally bold fiscal incentives to give motorists full confidence to switch,’ continued Hawes.

‘We welcome the changes made today as a step in the right direction for the UK automotive sector. However, it is vital that more incentives are available to encourage the consumer to move to EVs,’ stated CEO of the National Franchised Dealers Association (NFDA) Sue Robinson.

‘The EV targets remain in place and the fines remain too high for manufacturers. The UK remains the most aggressive regime for the EV transition, and we would want the UK Government to align with the rest of Europe, to make our market as competitive as possible in a rapidly changing global marketplace,’ she highlighted.

While outlining amendments to the ZEV mandate and 2030 new-ICE ban, it has stopped short of announcing incentives for the purchase or ownership of an electric vehicle. At the recent SMMT Electrified conference, calls were made for a reduction in VAT on public charging to benefit those without access to off-street parking.

There were also calls for the Expensive Car Supplement (ECS), applicable to vehicles registered from 1 April, to be raised by £20,000 to £60,000 to avoid it impacting the ZEV market.

The ECS will see £425 added to the standard vehicle excise duty (VED) rate in years two to six of registration, with EVs having been previously exempt.

Best month for BEVs

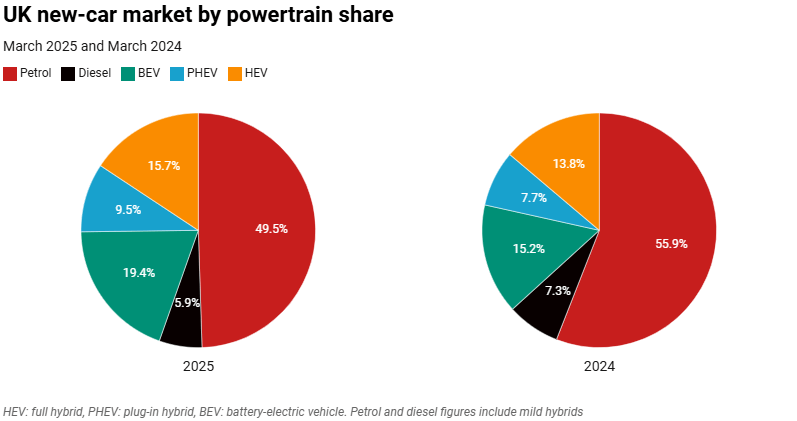

Battery-electric vehicles (BEVs) led the market in terms of registration improvement in March. The 69,313-unit total was 43.2% higher than the same month in 2024. This equated to a rise of 20,925 units year on year. This was the largest ever monthly volume for the powertrain.

However, the SMMT reports that manufacturers offered significant discounting, as they sought to deliver more ZEVs to drivers during the new ’25 plate’ month. As March usually accounts for around 16% of annual registrations, it was important to have as many deliveries as possible, to count towards their ZEV mandate targets.

Furthermore, the introduction of VED from 1 April could impact the market. This regulation will see a £10 tax during the first year of registration, rising to £195 annually. Additionally, new BEVs registered on or after 1 April will be eligible for the ECS if they cost more than £40,000. This may explain the higher March figures, with drivers aiming to avoid that charge.

The increase means that the all-electric technology’s market share jumped by 4.2pp to 19.4%. It was the second-best powertrain in the month, ahead of HEVs but some way behind petrol.

Yet, this share, while significantly improved, is 8.6pp behind the 29% ZEV mandate target for this year. With the VED and ECS changes, figures may struggle to reach the required figure.

In the first quarter, BEV registrations have increased by 42.6% This was thanks to the push and discounting by manufacturers. A total of 120,191 units have taken to UK roads, with a 20.7% share of the year-to-date total up 5.2pp year on year.

Hybrid growth continues

Unlike other European markets, the SMMT mixes mild-hybrid registrations with their equivalent petrol and diesel counterparts, This means figures for the hybrid market are based on HEVs and PHEVs.

HEVs achieved a rise of 27.7% in March, with 56,161 registrations. This led to a 15.7% market share in the month, up by 1.9pp. In the first quarter, the powertrain was up 18.7%, with 86,005 units delivered. This was a 14.8% hold of the total across the first three months of 2025, up by 1.5pp.

Meanwhile, PHEVs saw a growth of 37.9% year on year, albeit on smaller volumes. Their improvement in March meant 33,815 models took to the road. The powertrain captured 9.5% of the market, up from its 7.7% share recorded a year previously.

Between January and March, PHEV registrations rose 26.1% with 53,686 registrations, giving it a 9.2% market share. This was up 1.4pp year on year.

Grouping BEVs and PHEVs together, the EV market saw figures up by 41.5% in March, an improvement of 30,233 units. In the year to date, numbers were up by 37%. Plug-ins accounted for 30% of overall deliveries, up from a 22.9% share recorded in the same period of 2024.

Adding HEVs into the mix, the electrified market grew by 36.3% in the third month of 2025, with 159,289 new units leaving forecourts across the country. However, its 44.6% market share was not enough to dislodge ICE as the dominant powertrain technology. Over the first quarter, electrified registrations were up 30.4%.

Petrol proves popular

Petrol cars, including mild-hybrids, continued to lead the market in March. However, the 176,847-unit total was down 0.4% year on year, a difference of just 738 units.

The performance was the best of the year for the powertrain, following double-digit losses in January and February. It meant that petrol accounted for 49.5% of the market, although this was a drop of 6.4pp compared to March 2024.

In the first quarter, petrol registrations fell by 7.1%. The performance in March helped to reduce this loss, which stood at 16.1% over the first two months of the year. A total of 286,787 units were delivered, taking 49.4% of the total. This is a drop from the 56.6% share recorded in the first three months of 2024.

Diesel was both the least popular and worst-performing powertrain in March. The 20,967-unit total was 10.1% down year on year. Meanwhile, its 5.9% market share was 1.4pp off its hold in March 2024.

Over the first three months of the year, diesel deliveries have declined 10.2%, with 33,833 units. The powertrain’s market share of 5.8% is down from the 6.9% held at the same point last year.

Combined, ICE registrations in March fell just 1.5%, or 3,083 units. The group made up 55.4% of the market, a drop of 7.8pp year on year. In the first quarter, ICE deliveries fell 7.4%, with its 55.2% hold down from the 63.5% recorded during the same period of 2024.

This content is brought to you by Autovista24.