Close

CloseJayson Whittington, head of valuations in the UK for Glass’s (part of Autovista Group) discusses how residual values (RVs) have developed in the UK so far in 2023.

Demand for used cars has not dampened in the UK, despite consumers experiencing significant financial pressures due to the rising cost of living. Retail activity in the first quarter of 2023 was buoyant, which in turn led to busy wholesale channels as dealers sought to replenish stock more frequently.

At auction houses, demand outstripped supply throughout March, which led to Glass’s average RV for a three-year-old car to increase by 1.4% in April, according to Autovista Group’s monthly market dashboard. A year-on-year comparison shows that RVs have increased by 5%.

There was a difference in fuel types when it came to RVs in April however. Petrol cars experienced a greater increase of 2%, while diesel values rose by 0.7% and hybrid models grew by 2%. Only plug-in vehicles bucked this upward trend, with plug-in hybrids (PHEVs) falling by 0.1% and battery-electric vehicles (BEVs) falling 9.7%. BEVs now sit 14.1% lower than they did in April 2022.

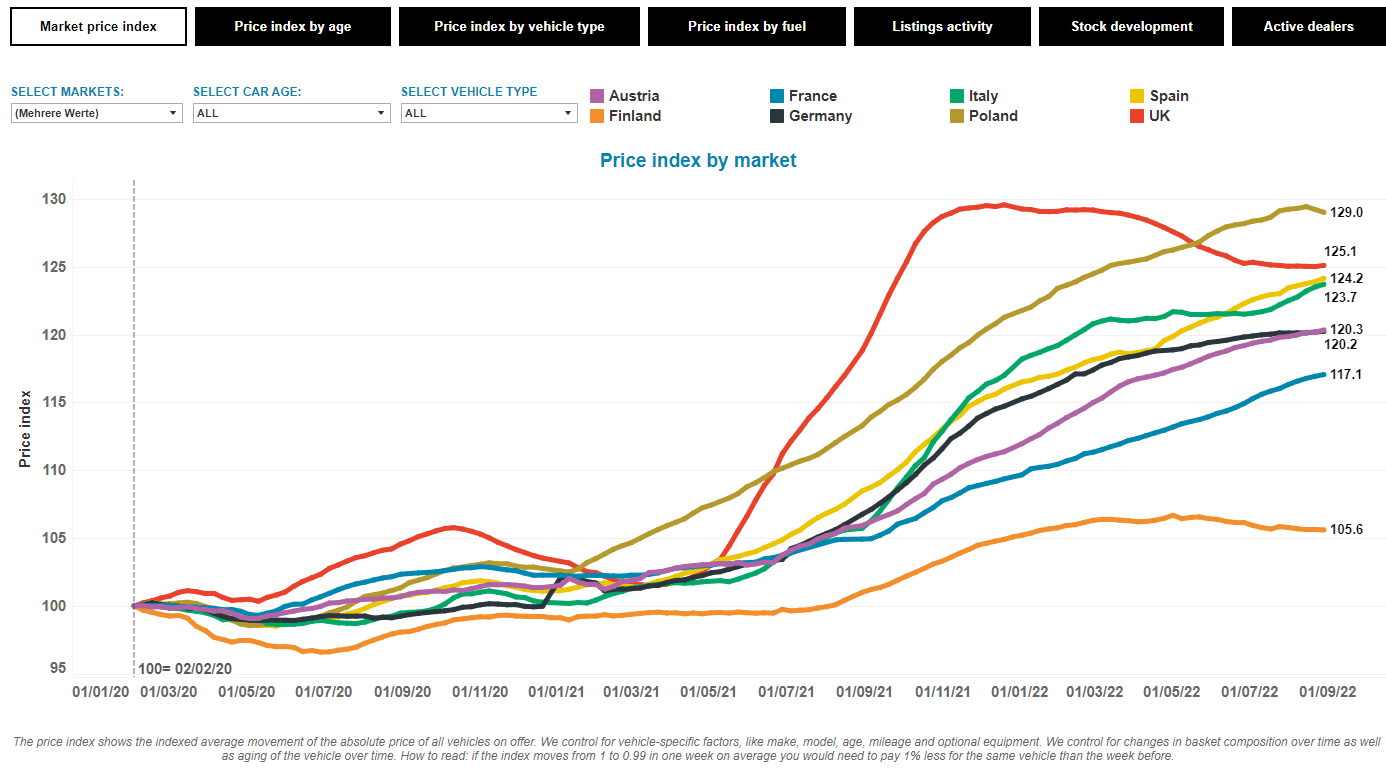

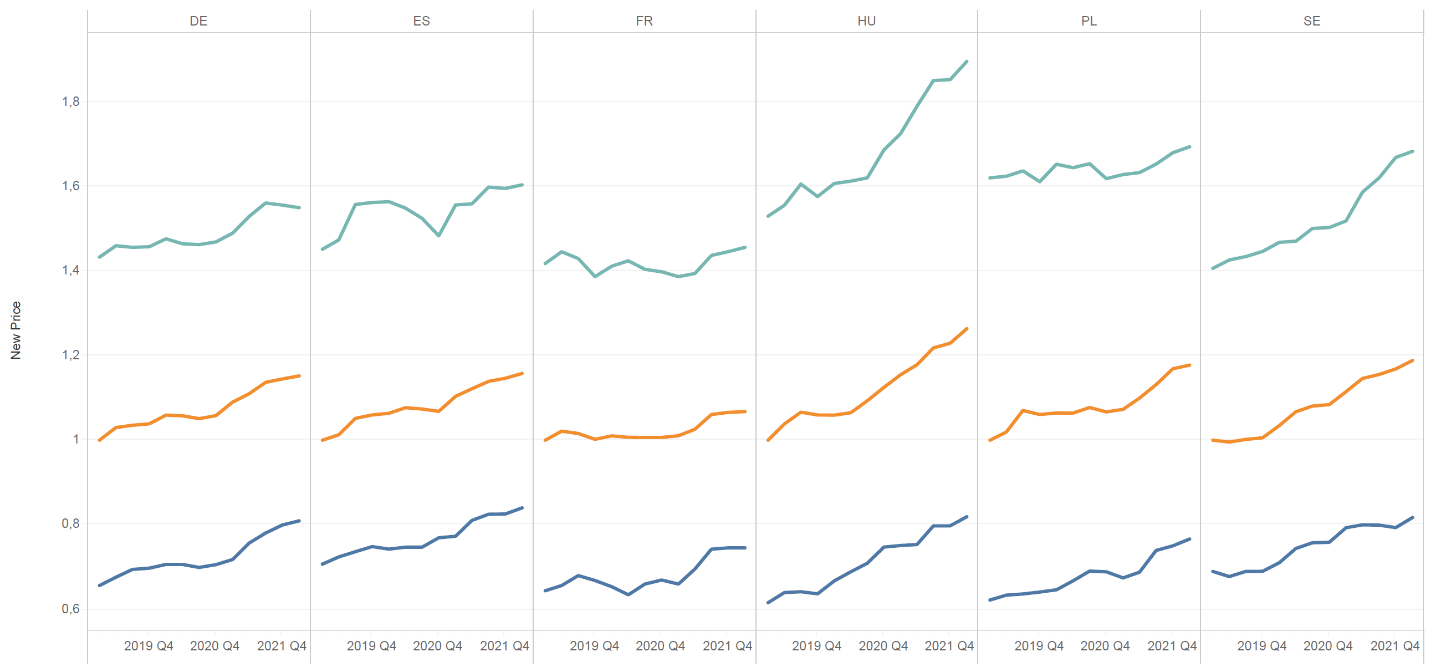

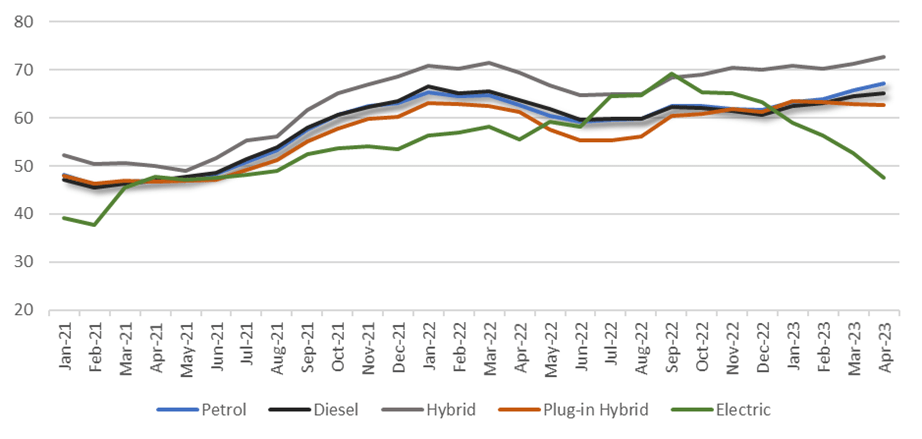

The chart below shows the development of residual values as a percentage of retained list price (%RV) since January 2021, split by fuel type. All RVs rose significantly as the market began to experience strong retail conditions coupled with reduced used-car supply throughout 2021. This was the result of severe delays in new-car production caused by COVID-19-related labour and component disruption, which saw fewer used cars enter the market due to contract extensions and a smaller number of part exchanges.

%RVs of 36-month-old cars by fuel type, January 2021 to April 2023

BEVs struggle on used-car market

It appears the used-car market began to correct downwards from the second quarter of last year but recovered again as supply eased once more. Except for BEV models, values have been relatively stable ever since. While BEV values have fallen sharply since the final quarter of 2022, the average RV remains higher than in January 2021, due to the upward trajectory experienced throughout 2021 and 2022, thanks to high demand and poor supply.

Hybrid models continue to outperform all other fuel types, retaining a greater percentage of original cost price at three years of age. At 72.7%, values are a staggering 25 percentage points higher on average than BEV models, which are currently performing the worst. Although, for context, the difference is only £391 (€450), in favour of BEVs, and perhaps that underlines a part of the issue.

BEVs are far more expensive to buy when new than other fuel types. However, the used buyer is not prepared to pay a large premium for a vehicle that offers few benefits over internal-combustion engine (ICE) and hybrid alternatives, plus they are no longer in short supply.

There remains very good retail demand for used BEVs, demonstrated by Autovista’s sales-volume index which measures the level of retail sales. It shows a massive sales increase of 276% compared to April last year. However, demand is failing to keep pace with the huge increase in supply.

Selling BEVs takes dealers longer

The average number of days it took a dealer to sell a used car reduced in April, falling 1.8 days to 38 days. This was almost two weeks less than 12 months ago, underlining just how buoyant retail activity has been. PHEVs and BEVs took much longer for dealers to sell at 49 and 53 days respectively, with hybrids taking 40 days, diesel 39 days and petrol leading the way at just 36 days.

The length of time it takes to retail a BEV will be a concern to dealers. At 53 days, that is 15 longer than the average, which brings with it an additional potential risk in the form of two costly book drops. It is therefore easy to understand why dealers have become cautious and auction hammer prices have been in decline. It is likely that rather than keep BEVs in stock, dealers will wait for a commitment from consumers before buying from wholesale channels, especially as there is no shortage of BEVs on offer.

Changing expectations

At the beginning of the year, Glass’s expected the rising cost of living and further planned increases in energy costs to have a negative impact on used-car sales and RVs by year-end. It was anticipated that RVs would decline by around 5%, following on from last year’s fall of 2.5%. Even with this fall, the value of used cars would remain high due to the approximately 30% rise in RVs in 2021.

However, with demand outstripping supply and no obvious increase in stock on the horizon, this expectation has changed, with values now anticipated to end the year in line with December 2022. There will of course be exceptions to this, in particular BEVs, where supply continues to outstrip demand and values remain volatile.

This content is brought to you by Autovista24.